从人口结构看,中国房价将在2050年回到2007年水平

文章来源: 财经杂志

11/14/2021

人口红利的消退(老龄化与少子化)是中国乃至全球经济增长面临的长期、刚性约束。历史上,战争、饥荒、病菌和自然灾害等是影响人口数量与结构变化的重要因素。二战后的和平发展与技术进步使人类在很大程度上克服了各类“生存危机”,平均预期寿命显著提升。随着战后“婴儿潮”一代渐渐步入老龄化,曾经的人口红利转变为“人口负债”,这对经济增长和大类资产价格有深刻含义。

中国的人口红利“来得快,去得也快”。在中国居民资产配置结构中,房地产尤为重要。西方国家近百年的经验显示,房价与人口红利(生产者/消费者,即劳动年龄人口/非劳动年龄人口)总体呈正相关关系。本文根据未来30年中国人口结构的变化趋势,估算了其对房地产价格的影响。结果显示,假定其他条件不变,截至2030年和2050年,人口结构变化将分别使中国实际房地产价格下降约6.71%和20.1%,分别回归到了2016年和2007年的水平。

在居民资产配置中,房地产占比与劳动年龄人口占比呈正相关关系。本文估算的结果显示,代表性中国家庭总资产中的20.71%(约23.7万元)需进行再投资,意味着全国当下共有约117.12万亿元的资产总量需进行再配置。

人口与地产价格:100年特征事实

相比于其他经济因素,人口如草灰蛇线,隐于不言,细入无间,暗藏于经济的变动中。人口及其相对结构是一个慢变量,但其对资产的影响并不是慢速线性外推的,人口结构中蕴含着的经济增长、风险、债务等宏观经济力量往往会在人口转折期突然释放,引起资产价格的波动放大(彭文生,2013)。

作为大类资产的重要类别,地产的特殊属性和地位源于其与金融系统的密切联系,从地产的分析视角出发,虽然流动性、土地供应等因素会在一定期间内掩盖长期趋势,但人口变迁是难以改变的趋势性力量,地产的周期变化本身就与人口密切相关。

人口增长催生的包含建筑、水泥在内的“人口敏感型投资”(Kuznets,1930)构成了库兹涅茨周期,继而触发经济、总供给的周期性波动。

对于房地产而言,关键的人群是劳动年龄人口,放在长周期来看,人口总量很重要,但人口结构对房地产更加重要,不同年龄组人群对应着不同水平的地产需求。

劳动年龄人口是经济生产的主力,也是房地产需求的主力。而人口经济学中的非劳动人口则会对劳动生产率、资本形成和储蓄率产生负面影响(Choudhry等,2016)。把年龄在15岁-64岁之间的人口定义为生产者(也称为抚养者),15岁以下和65岁以上的人口定义为消费者(即被抚养者),生产者/消费者的比值越高,意味着人口红利越丰富,劳动生产力越高,抚养负担更小。

劳动年龄人口对地产的需求有直接或间接两种渠道,直接是指个人房地产购买与配置需求;间接是指通过支撑经济增长的方式作用于房地产价格。常被忽视的是居民资产配置对房价的影响:在人口红利丰富时期,劳动力供给充足,储蓄上升,资金条件充裕,投资率也更高,为经济增长提供了额外的源泉,从而也对地产价格形成了支撑。

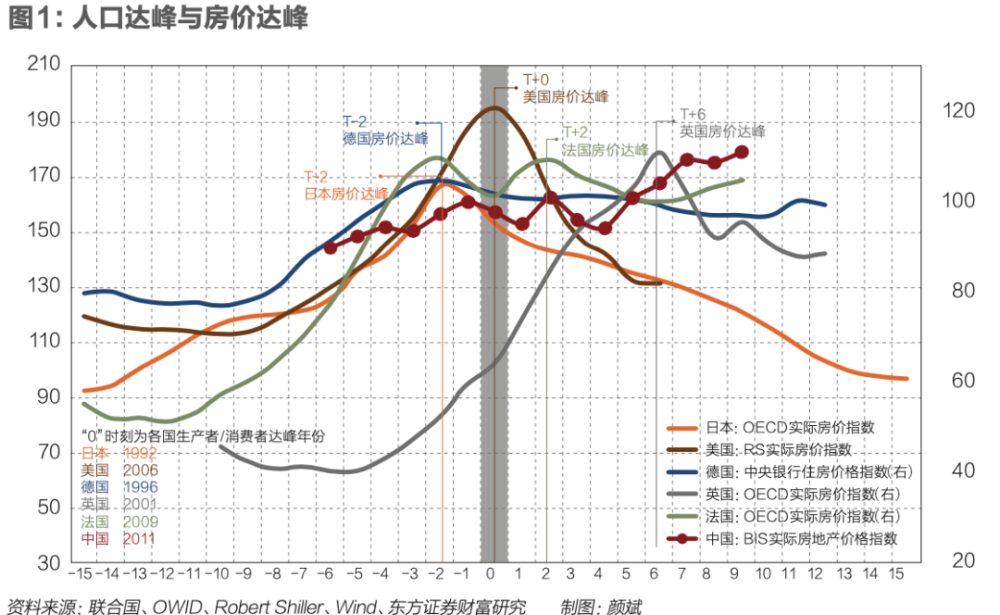

分析美国、日本、韩国、德国、英国、法国近100年来的人口-房价的经验关系,我们总结出三项特征事实。

房地产价格的上涨主要发生在生产者对消费者比值的上升期。虽然细节不尽相同,房价与人口结构并不完全同步,但各国房地产价格的上涨与生产者相对比重上升离不开关系。典型的如日本20世纪80年代、欧洲90年代,美国21世纪初。

地产价格的下跌一般对应生产者对消费者比值的下降。生产者/消费者比值下跌,对应了人口红利的消退,削弱了地产配置需求与经济的增速,典型的如美国的20世纪60年代,日本2000年以后的时期。

人口红利达峰期前后,房地产价格波动性增加。

典型的是日本20世纪70年代与90年代、美国2008年前后、德国2000年前后。美国、德国、法国、英国、日本的房价在人口红利达峰前后的6年内均出现了较大的波动。人口结构转折对地产的负面影响并不完全是住房需求衰退导致的,人口结构达峰对应的往往是经济中债务风险、经济增长逻辑的转变,这导致房地产下跌力量的集中释放。

美国。1900年以来,以生产者/消费者超过2(抚养比低于50%)为标准,美国共出现了三轮人口红利期,两轮人口负债期。

人口红利期均对应着房价上涨,人口负债期均对应的是房价的下行。

第一轮房价上涨时期是20世纪30年代至50年代初,美国出现约20年的人口红利期,实际房价上涨约68%。第二轮上涨时期是70年代初至80年代末,战后婴儿潮进入劳动市场,劳动人口增加,通胀缓解,经济增速上涨。第三轮上涨时期是90年代末至今,这一阶段回声潮人口步入劳动市场。

从房价下跌期来看,两轮房价下跌期分别在1900年至1929年之间和50年代中后期至70年代初,美国均处于长期的人口负债期,后者更是美国20世纪规模最大的人口负债期,伴随着人口负担增加,60年代经济增速放缓,70年代通胀抬升,都压制了地产实际价格上涨。

美国人口结构达峰前后地产价格的震荡往往加剧。

最明显的是1989年和2008年,分别发生了储贷危机和次贷危机。人口红利时期积累的储蓄、债务杠杆无法得到持续支撑,即便不是直接导火索,人口也构成了美国地产危机的底层逻辑。

需要强调的是疫情以来房地产价格的异常攀升。

2020年,美国房地产价格上涨约10.2%,超过了2006年时期的峰值,但与2006年相比,美国生产者/消费者已处于下行期,人口抚养比已上升至50%以上。

参考美国的房价历史,每一轮人口红利进入人口负债的转换期都出现了房地产价格的震荡。第五次康波周期以来,资本账户开放和金融全球化导致全球房地产价格同步性增强,风向标就是美国地产市场,美联储货币政策变化有显著的外溢效应,当美国的金融条件发生变化或逆转,房价风险将传导至中国市场,随着美联储非常规政策退出的脚步渐行渐近,国内需保持相对克制的流动性条件。

劳动年龄人口对地产的需求有直接或间接两种渠道,直接是指个人房地产购买与配置需求;间接是指通过支撑经济增长的方式作用于房地产价格。常被忽视的是居民资产配置对房价的影响:在人口红利丰富时期,劳动力供给充足,储蓄上升,资金条件充裕,投资率也更高,为经济增长提供了额外的源泉,从而也对地产价格形成了支撑。

分析美国、日本、韩国、德国、英国、法国近100年来的人口-房价的经验关系,我们总结出三项特征事实。

房地产价格的上涨主要发生在生产者对消费者比值的上升期。虽然细节不尽相同,房价与人口结构并不完全同步,但各国房地产价格的上涨与生产者相对比重上升离不开关系。典型的如日本20世纪80年代、欧洲90年代,美国21世纪初。

地产价格的下跌一般对应生产者对消费者比值的下降。生产者/消费者比值下跌,对应了人口红利的消退,削弱了地产配置需求与经济的增速,典型的如美国的20世纪60年代,日本2000年以后的时期。

人口红利达峰期前后,房地产价格波动性增加。

典型的是日本20世纪70年代与90年代、美国2008年前后、德国2000年前后。美国、德国、法国、英国、日本的房价在人口红利达峰前后的6年内均出现了较大的波动。人口结构转折对地产的负面影响并不完全是住房需求衰退导致的,人口结构达峰对应的往往是经济中债务风险、经济增长逻辑的转变,这导致房地产下跌力量的集中释放。

美国。1900年以来,以生产者/消费者超过2(抚养比低于50%)为标准,美国共出现了三轮人口红利期,两轮人口负债期。

人口红利期均对应着房价上涨,人口负债期均对应的是房价的下行。

第一轮房价上涨时期是20世纪30年代至50年代初,美国出现约20年的人口红利期,实际房价上涨约68%。第二轮上涨时期是70年代初至80年代末,战后婴儿潮进入劳动市场,劳动人口增加,通胀缓解,经济增速上涨。第三轮上涨时期是90年代末至今,这一阶段回声潮人口步入劳动市场。

从房价下跌期来看,两轮房价下跌期分别在1900年至1929年之间和50年代中后期至70年代初,美国均处于长期的人口负债期,后者更是美国20世纪规模最大的人口负债期,伴随着人口负担增加,60年代经济增速放缓,70年代通胀抬升,都压制了地产实际价格上涨。

美国人口结构达峰前后地产价格的震荡往往加剧。

最明显的是1989年和2008年,分别发生了储贷危机和次贷危机。人口红利时期积累的储蓄、债务杠杆无法得到持续支撑,即便不是直接导火索,人口也构成了美国地产危机的底层逻辑。

需要强调的是疫情以来房地产价格的异常攀升。

2020年,美国房地产价格上涨约10.2%,超过了2006年时期的峰值,但与2006年相比,美国生产者/消费者已处于下行期,人口抚养比已上升至50%以上。

参考美国的房价历史,每一轮人口红利进入人口负债的转换期都出现了房地产价格的震荡。第五次康波周期以来,资本账户开放和金融全球化导致全球房地产价格同步性增强,风向标就是美国地产市场,美联储货币政策变化有显著的外溢效应,当美国的金融条件发生变化或逆转,房价风险将传导至中国市场,随着美联储非常规政策退出的脚步渐行渐近,国内需保持相对克制的流动性条件。

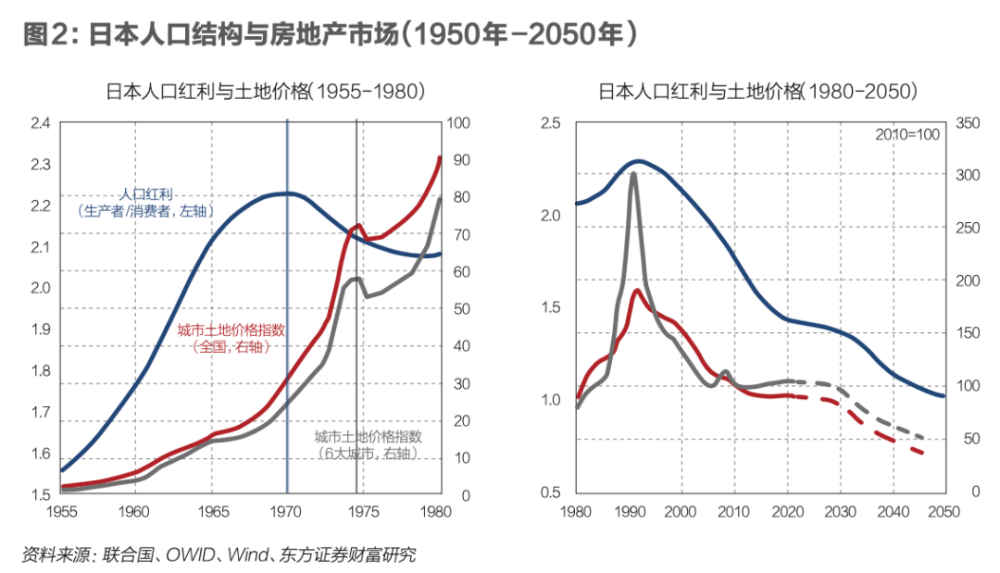

日本。日本地产随着人口结构的变化,出现了较为典型的两轮上涨和下行周期。

日本地产价格的上涨期分别出现在20世纪60年代至70年代初以及80年代,共性是生产者对消费者比值上升,劳动力充足,投资上涨,经济高速增长。1955年至1970年,日本年均GDP增速达到9.6%,80年代更是日本的黄金十年,居民地产直接配置需求与经济上升预期的螺旋共振,对房价形成了极高的支撑力量。

日本两轮房地产价格下跌期均对应了生产者/消费者比值的下跌期。第一轮较短的房价下跌发生在20世纪70年代中后期,第二轮房价下跌期发生在90年代后至今。70年代的短暂房价下跌后,市场能快速恢复的原因之一就是日本劳动人口依然能够支撑地产需求及价格。第二轮房价下跌的命运截然不同,1992年日本生产者/消费者比值达峰后开始持续下降,导致房地产的直接需求减弱,经济增长趋缓,到2018年房价已跌回1973年水平。

韩国。韩国的人口-地产关系与中国的接近程度更高,韩国同样实施了计划生育政策以及地产调控政策。

韩国1960年推出计划生育政策,早于中国约十年,虽在1996年结束生育控制,但韩国出生人口未能停止下行,到2020年生育率已跌至1以下。韩国同样实施了较为严格的房地产控制政策,20世纪70年代推出住房建设计划,80年代推出公租房、廉租房,90年代出台地产限价政策,2005年后开始征收房地产税,但依然阻挡不了韩国房价的上涨,背后的原因之一就是人口因素。

1987年,韩国人口结构由人口负债期转入人口红利期,抚养负担小于50%。整个80年代是韩国经济的黄金十年,劳动力充足,低工资、低汇率、年均经济增速超8.5%以上,虽然90年代末经历了亚洲金融危机的波动,但韩国地产价格上涨延续至今。韩国人口红利拐点早于地产价格拐点,但从韩国地产的建设端来看,2014年人口红利达峰后,韩国地产建设就已转入下行期。

德国、法国和英国的房地产价格与人口红利的正相关性更明显。

20世纪80年代初至1995年,德国生产者比重开始上升,尤其是1989年两德统一后,移民涌入,经济增速上涨,德国地产价格、建设经历了一轮较快的上涨期。1996年后,德国劳动人口比重下跌,至2008年降至局部低点,地产价格也下跌了约10%。2008年之后,德国生产者对消费者比值重新开始上升,德国的房地产价格也在同步上升。

法国与英国的人口周期变化较为接近。两国在20世纪世纪80年代-90年代人口红利上升,经济高速增长,房地产价格也出现了较快上涨,到2008年前后,英法的生产者/消费者值相继达到峰值,两国地产价格的波动也有所加大,尤其是法国的地产销售量与价格的背离出现加深。

中国案例:人口红利与房地产市场

相比海外经验,中国有相似之处,也有特殊性。相似之处是,中国与美国、日本等国家类似,也出现了二战后的婴儿潮,形成了房地产需求与经济阶段性高增长的内生力量。中国的房价上涨时期总体也对应了人口红利的增长期。

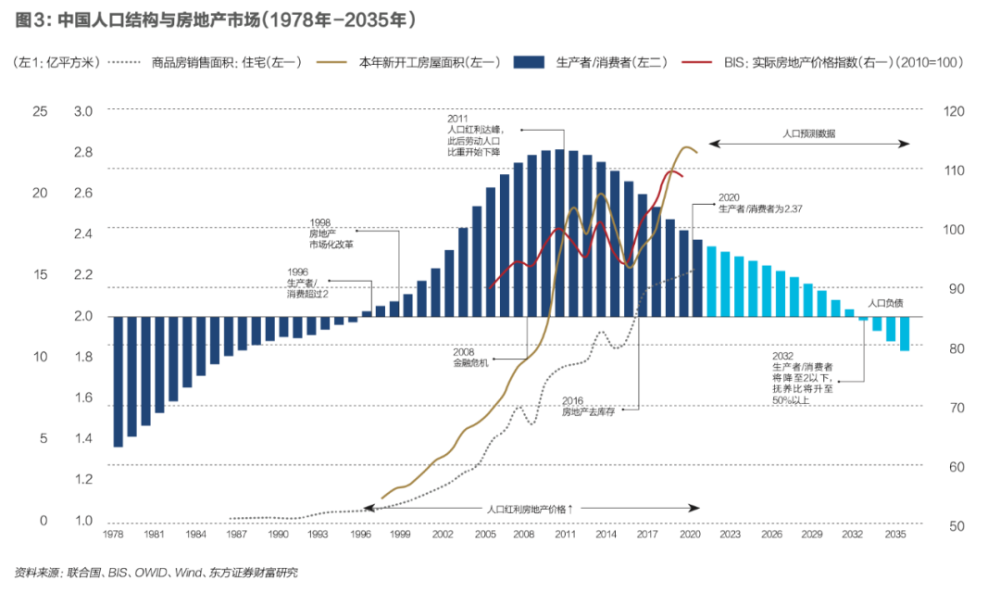

特殊之处,首先是中国房地产的市场化改革时间晚于住房需求的增长期,导致两批婴儿潮人口集中涌入地产市场,中国房地产市场化改革始于1998年,但20世纪60年代婴儿潮人口的住房需求在70年代末已经十分紧张,居民的住房需求释放被推迟十余年。二是中国通过人口生育政策只形成了一轮较高的、单峰的人口红利期。日本、美国、德国等国的生产者/消费者比值都具有双峰特征,这促成了中国经济、房价的长期高速增长。中国的人口红利,源于自60年代出生人口高增长,以及70年代、80年代的生育控制,劳动力快速增长的同时儿童抚养负担降低,在2000年后形成了集中型人口红利。人口红利本质是跨代际的资源转移,是当代人对未来的负债消费,将本应用来生育的投资改用于当代的生产及消费(陈友华,2005),当期经济实现了高增长,对房价形成了强支撑,但单峰的人口红利意味着中国未来的人口衰退会更加猛烈。

从人口角度观察中国房地产市场,有两个特殊的时期。第一个时期是1996年前后,中国生产者/消费者比值开始超过2,生产人口比重上升,由人口负债期转向人口红利期。60年代、70年代的婴儿潮人口达到劳动年龄旺盛期,成为经济高速增长、住房需求上升的推动力量。在需求推动及外部环境推动下,1998年,中国开始停止住房分配制度,建立商品房市场,中国房地产市场化改革的时间点与人口红利转化的时间点基本吻合。

第二个时间期是在2011年前后,中国人口红利达到顶峰,达峰的前十年是中国房地产价格快速上涨的时期,而度过人口红利高点之后,从总量层面看,中国房地产价格上涨也出现了波动,经济增速出现了调整与换挡。

可见,中国的人口与房价并未完全跳出一般性规律。但由于中国人口-地产关系的特殊性,房地产市场分配机制晚于人口红利上涨期,两轮婴儿潮人口在21世纪初集中进入住房需求市场,加上单峰型人口红利形成经济增速与房价的长期上涨,导致房地产达峰时间晚于人口达峰时间。

从人口看未来30年中国房地产价格

消费者人口(非劳动人口)中有两组人群:老年人口与儿童。从人口经济学的角度看,这是两组经济含义完全不同的人群。儿童随着时间的推移总能成长为劳动人口,历史上在婴儿潮出生高峰后,虽然社会的抚养负担短期内会加重,形成人口负债,但儿童为主的人口负债是具有生产性的,总能在未来转化为人口红利。

但老年人群体不同,老年人口是无法返老还童再次成为劳动力人口的,随着时间的流逝,老年人口的人力资本存量会折旧殆尽。老年人口占比提高会形成非生产性的人口负债,这种情况下人口负债是很难转换为人口红利的。

未来与历史的人口结构相比,最突出的转变就是消费者人群中,老年人口占比上涨,未来的50年很难再出现过去50年里人口负债向人口红利转移的现象。

美、英、德、法、日、韩等国的生产者对消费者比重都将持续性下跌,中国的生产者/消费者比值预计将在2030年降至2以下,预计到2050年降至1.48,意味着中国人口的抚养比将达到67%,100名劳动人口须抚养67名老人或儿童。

未来人口结构的变化对房地产而言,导致的直接后果是价格将持续承压。BIS在2010年借助全球22个国家约40年的人口与房地产价格数据,分析了人口对房价的影响。其研究显示,老年抚养比(老年人口占劳动人口的比重)上升会对房地产价格产生显著的负面作用,老年人口抚养比每提高1%,房地产实际价格将降低0.6%。

BIS通过该模型,结合联合国未来50年的人口预测数据,推算了未来人口变化对房价的影响。到本世纪中叶,人口结构中老年抚养比的加重将使各大经济体的房价下跌约20%到120%不等,美国下跌约25%,韩国降幅最大约120%,中国的降幅达95.8%。

不过由于联合国人口预测数据的更新、样本采样等问题,BIS的估计结果明显偏高。

我们参考BIS的方法重新进行了模型构建,进行了采样调整和固定效应修正,以生产者/消费者比值反映人口结构的d变化。我们的模型显示,生产者对消费者比值每下滑1%,实际房地产价格会下滑0.55%。

中国到2030年,生产者/消费者比值的下降会使实际房价下跌约6.71%,到2050年会使实际房价下跌约20.1%。在其他因素不变的条件下,这意味着实际房价在2030年将回到2016年的水平,在2050年将回到2007年的水平。

中国地产配置的长趋势

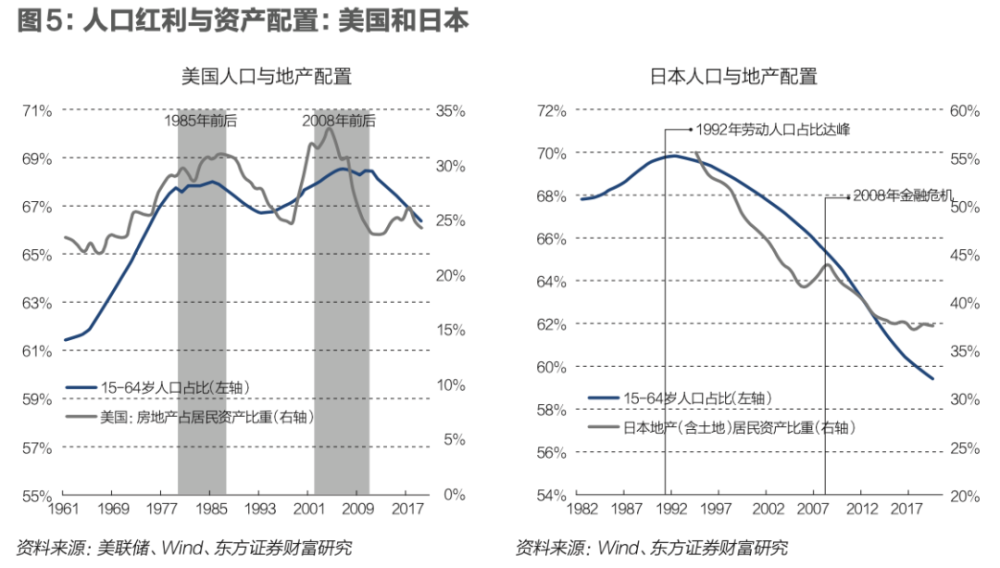

从生命周期的角度看,典型的个体追求的是其生命周期内一生效用的最大化(Modigliani和Brumberg,1954)。由于收入与消费的不匹配,个人一生在不同阶段倾向于配置不同类型和风险特征的资产,并调整风险资产的配置比重。从微观视角看,劳动年龄阶段的人口住房配置需求处于一生中的最高峰。反映到宏观层面,则意味着房地产配置比重也会与人口结构呈现正相关性。社会劳动人口比重上涨,进入住房市场的人口增速远远超过65岁以上人群离开住房市场的速度,需求流入量大于流出量,推动地产配置比重上涨。反过来,当老龄化程度上升,劳动年龄人口比重下降,房地产市场中流出的人口大于流入的人口,表现为地产配置比重的回落。

从1960年至今,美国居民部门的地产配置比重总体上与劳动年龄人口比重正相关,美国居民配置房地产有两次高峰,分别为20世纪80年代和2007年左右,两轮配置高峰对应了美国劳动人口占比的高峰期。

日本劳动人口比重在1992年前后达峰,此后地产的配置快速下滑。

德国与英国显示出了相似的趋势,德国劳动人口比重有两个高峰,分别在1996年前后和2010年前后,居民重配房地产的高峰也出现在这两个时期。英国劳动人口比重的上升期与房地产配置的上升期基本对应,在2002年后英国劳动人口比重逐渐稳定,居民配置房地产的比重也基本维持在45%左右。

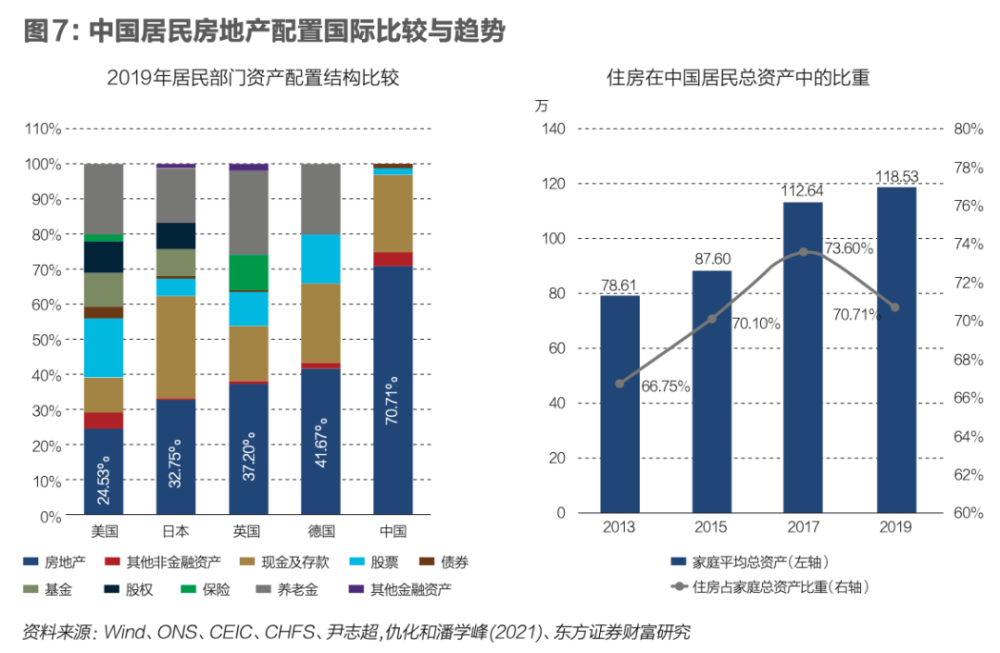

中国的资产配置研究中,并没有一般公认的数据显示居民配置地产的比重,但存在几项数据可供参考。一是央行2019年10月公布的城镇家庭资产调查,显示住房占家庭总资产的比重为59.1%。二是社科院国家资产负债表数据显示2019年住房资产占家庭总资产比重为40%。三是广发银行联合西南财经大学发布的《2018中国城市家庭财富健康报告》显示,中国家庭住房资产在家庭总资产中占比77.7%。我们此处使用中国家庭金融调查中心(CHFS)的数据,该数据显示,2019年中国居民房地产的配置比重为70.71%,典型家庭的平均资产总额为118.53万元。

从2019年国外居民部门房地产配置结构来看,日本居民配置房地产的比重约在32%,美国的比重约为24%,德国为41%,英国为37%左右,中国的地产配置明显偏高,以房地产配置比重由70.71%降至50%为标准进行估算,普通中国家庭总资产中的20%,约23.7万元需要从房地产市场中剥离进行再配置。2020年中国第七次人口普查数据显示,中国共有家庭49416万户,加总至宏观层面,意味着全国当下共有约117.12万亿元的资产在未来十年内需进行再配置,否则将可能面临资产消融的可能。

CHFS的数据显示2019年中国家庭配置房地产的比重已出现下降,相比2017年降低了3个百分点。人口是难以逆转的趋势力量,过去十余年的重仓配置使购房人群获得了巨量的财富增值效应。而资产配置的路径依赖会导致投资行为调整的滞后,理论上居民资金从地产中抽离是一个缓慢释放调节的过程,但国外的经验显示房地产配置的调整往往是源自债务风险的突然释放,表现为资产消融的形式,由于中国的人口红利下滑迅猛,中国房地产无法避免地存在下行压力,这将会影响未来30年以上的居民财富效应。

需要强调的是人口也并非决定房地产的唯一力量,人均GDP的提高能够对冲劳动人口收缩的负面作用。提供新的经济增长源泉拉动人均GDP增速上行与老龄化加速下行之间是一场关于时间的竞赛,取胜方不仅决定了房价,也决定了中国未来30年的经济前景。

邵宇为东方证券首席经济学家,赵宇为东方证券博士后,陈达飞为东方证券财富研究中心主管。

Kushner Real Estate Group Launches Leasing For 351 Marin Boulevard In Jersey City

BY SEBASTIAN MORRIS

11/13/2021

Leasing has officially commenced at 351 Marin Boulevard, a new 38-story rental property in Jersey City’s Powerhouse Arts District. Developed by Kushner Real Estate Group (KRE) and joint venture partner Northwestern Mutual, the property comprises 507 apartments. The mix of units includes studios and one- and two-bedroom homes.

Designed by Hollwich Kushner and HLW Architects, 351 Marin features a cleaved, cantilevered base that frames a 4,500-square-foot public plaza. From curb to cornice, the façade of the building comprises a mix of tan brick and large windows with black ventilation grills beneath.

Within the building, each apartment features wide plank hardwood flooring, in-unit washer and dryer, solar shades, steel appliances, and white quartz countertops.

Residents will also have access to an eighth-floor amenity deck with a 24-hour fitness center, a full entertainment kitchen with seating area, a movie and screening room, a game room, and a children’s playroom. On the same floor, outdoor amenities include a landscaped terrace with a pool, lounge seating, fire pits, and barbecues. A community garden and dog run can be found on the seventh floor.

A 37th floor sky lounge crowns the property and includes an outdoor, landscaped patio with a tiered theater and spectacular views of the Manhattan and Jersey City skylines. Indoor spaces include co-working areas and banquette seating.

“We’re excited to introduce 351 Marin to the public in a prime location in Jersey City just steps from the Grove Street PATH station and surrounded by dining, culture, and nightlife,” said Jonathan Kushner, president of KRE Group. “Our residents will be able to easily explore all that the city’s local fabric has to offer while also enjoying an elevated lifestyle at home enriched by a robust amenity offering.”

The Marketing Directors is the exclusive leasing agent for 351 Marin, where monthly rent for a studio unit is priced at $2,650 on the low end. Grand opening incentives include two months free on a 14-month lease and three months free on a 26-month lease. Initial occupancy is scheduled for December 1, 2021.

NJ Home Sales Cool, Prices Remain Hot for Fall

11/07/2021

High prices and low inventory have continued to cool sales throughout New Jersey. While New Jersey saw a slight decline in closed sales the past few months, overall sales are up 13.6% since the start of the year.

“For the past two years, the housing market has been an anomaly for a number of reasons,” said 2021 NJ Realtors President Jeff Jones. “The return to a more balanced market after almost a full two years of this competitive, in-demand atmosphere will be slower than potential buyers want and, likely, faster than those on the fence to sell will expect.”

Single family closed sales were down 17.5% in September 2021, to 7,756. Townhouse-condo closed sales were down 8.1% to 2,479, and adult community homes followed suit with a decrease of 14.4% to 729. Yet despite fewer sales, median sales price increased again across all categories in September. The single family median sales price increased 7.3% to $440,000; the townhouse-condo median sales price increased 5.1% to $310,000; and adult communities median sales price increased 26.4% to $303,330.

While listings are down year-over-year, the year-to-date new listings for all markets is down just 1.2% over the same period last year, which points to the market making up ground this fall, when new listings are typically lower.

The number of single family homes for sale remains low, but is still above the historical low of this past winter, which had the lowest number of homes for sale in over a decade, if not more. In September, there were 18,863 single family homes for sale throughout the state, representing a 26.1% decrease, which is typical of the decreases of the past three months.

Increasing inventory will be key to moderating prices, relaxing buyer competition, and opening the market back up. Many buyers have either been forced out due to affordability and not finding what they want leading them to wait. In a recent survey to 63,000 New Jersey Realtors, a majority of members see inventory as a very serious or serious problem, but with less intensity than when surveyed this past spring. Similarly, members surveyed said clients are not finding what they want within their price range, with just 41% reporting their clients are currently satisfied with the options in their price range.

If you know a potential first time homebuyer that is struggling to enter the market, have them visit newjersey.realestate/keys to register for a free virtual seminar to help potential first-time home buyers become homeowners. The seminar is this Thursday, Oct. 28 at 6:30 p.m. and all attendees will be entered to win a $250 gift card.

The $300m flip flop: how real-estate site Zillow’s side hustle went badly wrong

Zillow reportedly has about 7,000 homes that it now needs to unload – many for prices lower than it originally paid

11/05/2021

Online shopping can be dangerous, as the US property website Zillow has belatedly come to realize. While many of us wasted countless hours during the pandemic clicking through real estate listings on Zillow and daydreaming about the sort of pad we’d buy if we had deep pockets, the company was running a side-business, separate from its property searching website, in which it deployed algorithms to help it buy houses themselves and then flip them.

It did a lot of buying, but hasn’t been so great at the selling. This week the company announced that its home-buying division, Offers, had lost more than $300m over the last few months. Offers will now be shut down and about 2,000 people laid off. Zillow reportedly has about 7,000 homes that it now needs to unload; many for prices lower than it originally paid.

You would be forgiven for not knowing that Zillow was even in the business of buying houses. For most of its 15-year history the Seattle-based company focused on publishing online real estate listings. Then, in 2018, its CEO, Richard Barton, started to aggressively move the company into a business known as iBuying. The idea is that algorithms would identify attractive homes to flip; Zillow would buy the home directly from the seller; minor renovations would be made; Zillow would quickly flip the house and pocket a profit. At one point Barton aimed to buy 5,000 homes a month by 2024.

iBuying is a nascent industry. A recent report from Zillow found that the four largest iBuyers – Zillow Offers, RedfinNow, Offerpad and Opendoor – were responsible for just 1% of all US home purchases in the second quarter of 2021. (Although that number goes up to 5% in certain fast-growing markets like Phoenix.) But while it’s still in its infancy, there’s a lot of excitement among tech types about the future of algorithm-powered home buying. “There is an arms race right now of who will become the Amazon of real estate,” a real-estate professor at Columbia University recently told Marketwatch. “That’s why all these companies like Zillow or Redfin want to have everything in house.”

Enormous companies with deep pockets and mounds of data bidding against ordinary people in an already absurd housing market? It sounds like a nightmare for anyone who isn’t a tech investor. And indeed, news of what Zillow has been up to has caused a backlash on social media, largely fuelled by a viral TikTok by a Nevada real-estate agent called Sean Gotcher that claimed iBuyers manipulate the housing market.

Gotcher didn’t explicitly name Zillow but he heavily alluded to them and accused the company of using data harvested from people perusing their dream homes while they are bored on the website. Gotcher said this nameless company then buys a ton of properties in the neighbourhood people are searching for, and overpay for a couple of adjacent properties in order to artificially drive up prices. (Zillow and Redfin have denied doing this and real estate experts have noted they don’t have enough market share for this strategy to work.)

Zillow may not have been explicitly manipulating the market, but it was certainly trying to use technology to outsmart it. In the end, however, the market won. Zillow’s flipping flop should serve as a reassuring reminder that not everything can be automated. There are various reasons why Zillow got burned, including a labour shortage making it difficult to renovate homes. But the biggest issue is that its algorithm simply wasn’t up to snuff. It couldn’t deal with the complexities of pricing in a volatile market and resulted in Zillow overpaying for a lot of property.

While individual homebuyers may not have to compete against Zillow any longer, it’s unlikely that buying a house is going to get any cheaper or easier anytime soon. Those 7,000 houses Zillow is sitting on? Bloomberg reports that they will probably be offloaded to institutional investors like BlackRock rather than regular people. And while Zillow may be ending its iBuying business, the financialization of housing looks set to continue. Big money is gobbling up real estate and leaving many first-time buyers out in the cold.

Zillow helped drive up Triangle real estate prices, but its decision to exit could lead to deals

By Matt Talhelm | WRAL

11/03/2021

RALEIGH, N.C. — Zillow is trying to sell hundreds of homes it owns across the Triangle as the company gets out of the instant home buying, or iBuying, business.

The online real estate marketplace cited “unpredictability” in forecasting prices for its decision to halt iBuying.

WRAL News searched online property records and found Zillow listed as the owner of 211 homes in Wake County, 62 in Durham County, 41 in Johnston County and 10 in Orange County.

Zillow has been buying and selling homes in the Triangle for three years, and some in the real estate industry say the company has helped drive up home prices by routinely flipping homes days after buying them – sometimes for tens of thousands of dollars over what it paid.

“There has been a number of homes, probably the vast majority of them, that have been a bit overpriced,” Raleigh realtor Steve Gunter said.

Jeff Simerson sold his three-bedroom, three-bathroom home south of Garner to Zillow a month ago for $563,000, and the site now lists the property for $578,900.

“Everybody kind of looked at me funny when I said I sold my house to Zillow. They were like, ‘I didn’t know they were in real estate.’ I didn’t, either,” Simerson said.

He said his family needed to sell quickly to relocate to Florida, and Zillow made a cash offer $37,000 over his asking price.

“We just couldn’t understand where they were coming up with that number, because the comps in the area didn’t support the value they were offering me,” he said. “If I was going to still stay in Raleigh, I would have moved down the street to sell it for what they were offering us.”

Two other big iBuyers, Opendoor and Offerpad, own more than 400 homes combined in the Triangle, and a third, Redfin, recently announced plans to enter the market.

“They’re going to need to be very careful about how many homes they’re buying per month and where they are selling those homes from a price standpoint,” Gunter said.

Zillow officials said the homes it owns or is under contract to buy in the area will go through the company’s typical process to get them ready to list and sell.

But Gunter is telling his clients they could get a deal as Zillow winds down its sales operations.

“Whenever we have buyers looking to place offers in on those properties, we’ve just told them we’re going to need to offer less,” he said. “They are beginning to sell those homes for less than what they have paid for.”

Simerson said he’s glad he closed on the sale to Zillow when he did.

“If they buy it inflated in the first place,” he said, “they’re going to drop the price to what the market will sustain.”

房价太难料 Zillow蒙受巨亏 退出房屋交易业务

来源:美国中文网

11/02/2021

以估算房屋价值而闻名的房地产网站Zillow周二表示,在严重亏损的情况下,它将退出快速买卖房屋的业务,并计划解雇其近25%的员工。

这一宣布是一次重大的战略撤退,也是对Zillow首席执行官巴顿(Richard Barton)的一记重拳,他在16年前创建了该公司,并长期以来一直在努力将Zillow这个资讯网站转型为一个交易平台。去年,巴顿预测Zillow Offers可以创造200亿元的收入,这是通过一种被称为iBuying的做法对房屋进行即时买卖的操作。简单来说,iBuying是公司依靠技术手段,确定基于市场的现金报价,即时买下房屋的操作。

周二,Zillow表示该部门一直是巨额亏损的来源,并使公司的整体底线无法预测。Zillow Offers在截至9月的三个月内损失了超过4.2亿元,与该公司在之前12个月内的总收入大致相同。该公司拥有8000名员工。

巴顿在一份声明中说:”我们已经确定,房价的不可预测性远远超过了我们的预期。”

巴顿在周二下午与分析师举行的电话会议上说,这一决定对他来说”很重要”。巴顿说:”我们可以把目前的损失归咎于偶发的市场事件。但如果料定未来不会再发生不可预测的事件,那就太天真了。”

该公司在第三季度总共损失了近3.3亿元,这比华尔街分析师预测的要差得多。该公司在一年前的同一时期实现了4000万元的利润。

Zillow的股票已经从2月份近200元的高点下跌了50%以上,当时随着房地产市场的升温,它还是投资者的宠儿。周二,该股在发布财报前下跌了11.5%,至约85.50元,盘后交易中又下跌了7.5%。

三年前,该公司宣布计划采用其定价估算来购买和出售房屋。现在,Zillow持有数千套房屋,其价值低于该公司的买入价。

上个月,Zillow宣布它将暂时停止购买新房。当时,它把问题归咎于缺乏工人来修复和翻新所购买的房屋。但在周二,巴顿表示,使用其算法来买卖房屋并没有产生预测的利润。该公司现在正寻求抛售剩余的7000套房屋。

《纽约时报》评论称该公司似乎低估了持有房屋的风险。该公司此前还试图迅速将其房屋交易业务提高到每月5,000笔,这是巴顿设定的目标,而当时的住房市场库存已经很低,并开始降温。

Zillow, facing big losses, quits flipping houses and will lay off a quarter of its staff.

By Stephen Gandel

11/02/2021

Zillow, the real estate website known for estimating house values, said on Tuesday that it would exit the business of rapidly buying and selling houses amid heavy losses and that it planned to let go about nearly 25 percent of its employees.

The announcement was a major strategic retreat and a black eye for Richard Barton, Zillow’s chief executive, who founded the company 16 years ago and has long talked about transitioning Zillow’s popular website into a marketplace. Last year, Mr. Barton predicted Zillow Offers, which made instant offers on homes in a practice known as iBuying, could generate $20 billion a year.

On Tuesday, Zillow, which said it has 8,000 employees, said the division had been the source of huge losses and had made the company’s overall bottom line unpredictable. Zillow Offers lost more than $420 million in the three months ending in September, roughly the same amount that the company had earned in total during the prior 12 months.

“We’ve determined the unpredictability in forecasting home prices far exceeds what we anticipated,” Mr. Barton said in a statement accompanying its quarterly financials.

Mr. Barton, speaking on a conference call with analysts on Tuesday afternoon, said the decision had “weighed heavily” on him. “We could blame the current losses on exogenous market events,” Mr. Barton said. “But it would be naïve to predict that unpredictable events won’t happen in the future.”

In all the company lost nearly $330 million in the third quarter, which was far worse than Wall Street analysts had predicted. The company made a $40 million profit in the same period a year ago.

Shares of Zillow have fallen more than 50 percent from a high of nearly $200 in February, when it was still a darling of investors as the housing market heated up. The stock dropped 11.5 percent on Tuesday to about $85.50 before it released its financials, and a further 7.5 percent in after-hours trading. (Even so, Zillow’s shares are worth double what they were at the beginning of the pandemic.)

Three years ago, the company announced plans to employ its pricing estimates to buy and sell houses. Now, Zillow is sitting on thousands of houses worth less than what the company paid for them. Last month, Zillow announced it would temporarily stop buying new homes. At the time, it blamed a lack of workers to fix up and sell the houses it had bought. But on Tuesday, Mr. Barton said using its algorithm to buy and sell houses had not produced predictable profits. It is now looking to offload its remaining 7,000 houses.

It appears the company underestimated the risk of holding houses in between transactions, which was a departure from the low-risk, high-margin ad business. And it tried to quickly ramp up its home-flipping business to 5,000 transactions a month, which Mr. Barton set as a goal, in a housing market that was already low on inventory and was starting to cool off.

Zillow’s stumble also raises questions about its core product, which is built around its value estimates. Aaron Edelheit, who began buying houses in the wake of the Great Recession, tweeted his thanks to Zillow for paying “such an extremely high price” for one of his properties this summer. “It appeared they were panic buying,” Mr. Edelheit, who is leaving the real estate market to focus on cannabis, told The New York Times’s DealBook newsletter. “I didn’t get it. I should have shorted the stock.”

北美法律公益讲座安排

时间:周二到周五 晚间

5:30-7:00(西部)

8:30-9:30(东部)

重播:第二天

上午9:00(西部时间)

中午12:00(东部时间)

周二: 遗嘱和授权书(Lisa讲)

周三: 数据泄露和个人身份保护&事业机会说明会

周四:北美常见法律问题(讲员Irene )

周五:小企业法律和员工福利(晶旌)

Zoom 6045004698,

密码:请扫码进群

另外:周三6:30(西部时间)美国专场

定期邀请美国律师联合讲座

Zoom 951 9092 9213

密码:请扫码进群

Zillow’s iBuying flop: Company listed nearly two-thirds of homes below purchase price

Firm is pausing buying for rest of 2021

TRD Staff

11/01/2021

Questions over the profitability of Zillow’s iBuying practices in the increasingly competitive space appear to be close to the operation’s troubles detailed in an Insider analysis.

Insider examined the company’s listings on October 27 in five markets: Dallas, Houston, Phoenix, Atlanta and Minneapolis. The outlet found almost 64 percent of the homes were listed for sale for less than Zillow paid for them, with a median difference of $16,000.

Of the 963 listings Insider reviewed, 616 were being listed for less than Zillow’s purchase price. The problematic listings were particularly noticeable in Phoenix and Dallas, where 93 and 81 percent of listings, respectively, were below Zillow’s purchase prices, respectively.

Across the five cities, only Atlanta saw the problem occur less than 60 percent of the time; the low listings accounted for about 28 percent in Zillow’s largest metro of inventory. The cities make up nearly a third of Zillow’s entire inventory.

Oct 14, 2021

Zillow Business Model – How they have been disrupting the real estate market since 2006. How does Zillow make money, and what is the impact of their iBuying business on the real estate price inflation across the United States? Find it all out in this video.

Insider’s analysis came less than two weeks after Zillow temporarily shut down its iBuying program. The company claimed to be “beyond operational capacity,” stuck with a backlog of properties.

The pause marked the second time in two years Zillow has ceased its home-buying operation since its launch in 2018. Ongoing labor shortages and volatile material prices slowing down repairs and renovations of purchased properties likely contributed to its recent backlog of pending property sales.

Zillow Offers allows homeowners to receive an offer on their home through Zillow’s proprietary technology, which can allow for a quick offer and sale. After the transaction, the property receives minor repairs before it’s put back on the market.

Zillow reported making $1.5 billion in revenue from its iBuying business during the first half of 2021. Insider reports Zillow CEO Rich Barton has said the company could hit $20 billion in revenue from iBuying annually in three years.

The four largest iBuying companies combined to purchase 15,000 homes in the second quarter. Zillow has aspirations to surpass that figure, however, and purchase 20,000 homes on an annual basis by 2024.

Zillow will announce its third-quarter earnings on Nov. 2, potentially shedding light on the success and failures of its iBuying business.

Zillow炒房失利 近半上市房屋削价求售

世界新闻网

10/31/2021

面对美国史上增长速度最快的房地产价格,房地产商Zillow决定加强炒房(home flipping)业务;然而,这项策略让Zillow在今年第三季得标买下的物业数量创下有史以来最多的纪录,使他们不得不停止出价。

在Zillow处理需要整修再出售的物业之际,他们同时面临了一个不利的现实:房价上涨放缓,意味他们将亏本出售许多房屋。

根据YipitData的调查,Zillow 9月推出的上市房屋数量创下历史新高,却以2018年11月以来最低的加价幅度出售。事实上,在第三季,Zillow将近一半的美国上市房屋都削价求售,代表库存量过多迫使他们降低售价。

这个现象已经出现在房价不断飙涨的亚特兰大和凤凰城,Zillow凤凰城约250笔上市房屋目前的定价已比Zillow当初收购这些房屋时的价格低6%。

波德科罗拉多大学(University of Colorado Boulder)房地产科技策略家德尔普雷特(Mike DelPrete)说:「过去几个月来,我看到Zillow每一项主要指针都不合理,像是他们对市场做出的反应晚了两到三个月。」

根据德尔普雷特的分析,Zillow的主要竞争对手Opendoor虽然在凤凰城的房屋销售价差也开始缩小,但成交价仍持续高于收购价。Opendoor在亚特兰大的销售情况也十分出色,他们以高于收购价6.5%的定价挂牌出售房屋,相较Zillow的价差只有1.3%。

Zillow 10月18日表示,由于正在处理积压的物业,将暂停收购新物业,消息让Zillow股价下跌9.4%。尽管Zillow股价已回升,但分析师大多对其炒房策略的失误不以为然,并指出Zillow追溯到2018年的炒房业务至今尚未获利。

RBC Capital Markets分析师艾利克森(Brad Erickson)说:「他们可能有些措手不及,但或许不会太在意,在这个阶段,赚钱并非最主要的目的。」

Zillow和Opendoor都使用一种名为iBuying的高科技炒房软件算法来预测房价走势,每季收购成千上万笔物业。专家表示,这是一个复杂的过程,必须计算得非常精确才能获利。

Zillow和Opendoor向客户推销使用其服务的便利性,他们收取的费用取代了传统的房地产经纪人佣金。

Zillow’s flips flop, hurting profits but benefitting some homeowners

By Hannah Frishberg

10/31/2021

The streets aren’t being easy on Zillow, which is reportedly losing money on homes it bought to flip, but are instead proving flops.

The real estate company has paused its home buying operation, Zillow Offers, after an algorithmic tweaking to make higher home offers failed to keep up with the real estate market, Bloomberg reported this week. This resulted in Zillow overpaying for homes it couldn’t resell even for the sale price, let alone a profit, Bloomberg reported.

The failed buying spree has benefited some homeowners, who sold houses to the company at rates which turned out to be overmarket. These winners of the real estate fumble include seller Abidemi Bolatiwa, who sold his Phoenix four-bedroom to the company for $531,300 in late September, saving money on a Zillow convenience fee cheaper than what a traditional agent commission would have cost, according to Bloomberg. Zillow listed the property for $505,900 10 days later, but it didn’t sell, so the company cut the price to $494,900.

After a real estate agent made him a lower offer than Zillow, Richard Flor of the Phoenix suburb Tolleson, Arizona decided to sell to the company this summer. Zillow paid him approximately $412,000 and charged only a 1 percent fee on the sale of his three-bedroom, three-bathroom rental property. Two weeks later, after making light repairs, Zillow listed the property for $387,000 — $3,000 less than what the agent had offered.

On Oct. 18, Zillow announced it would stop making home buying offers, thus pausing the home-flipping program which has failed to turn a profit since being started in 2018.

“Prices turned on them and they got a little bit flat-footed and they were probably a little too aggressive on the bidding,” RBC Capital Markets analyst Brad Erickson explained to Bloomberg, regarding where Zillow’s market strategy failed. While a loss, though, the failure won’t hurt the company too badly. “They probably don’t care so much. It’s not as important at this stage of the game to make money,” Erickson added.

Zillow’s zeal to outbid for houses backfires in flipping fumble

Patrick Clark and Noah Buhayal | Bloomberg

10/27/2021

Faced with the fastest-growing real estate prices in US history, Zillow Group has tweaked algorithms to enhance home flipping operations to offer higher offers.

It ended up with so many successful bids that I had to stop offering new offers for the property. Now, after buying more homes than ever in the third quarter, the company is tackling the unprocessed portion of homes that need to be repaired and sold in the face of unpleasant reality. The slowdown in price increases has cost many homes.

According to a YipitData survey, Zillow launched a record number of homes on the market in September, listing properties with the lowest markup since November 2018. According to Yipit, in the third quarter, prices fell by almost half of the US listing, indicating that inventories are lower than expected.

The shift is on display in places such as Atlanta and Phoenix, two markets where home prices are skyrocketing. Zillow’s approximately 250 active list in Phoenix is now on average 6% cheaper than the company paid for homes.

According to data compiled by Mike Delprete, a real estate technology strategist and scholar at the University of Colorado at Boulder, this represents a $ 29,000 discount on typical real estate.

“All the key indicators from Zillow over the last few months are totally meaningless,” said Del Prete. “It’s like making a decision a couple of months behind the market.”

Zillow’s newly discovered aggression was good for people like Abidemi Bolatiwa who were watching the process run in real time. According to real estate records, he sold his four-bedroom home in Phoenix to Zillow in late September for $ 531,300, paying a convenient fee that was cheaper than traditional agency fees.

Mr. Volatiwa also Opendoor Technologies, That would have paid him about $ 504,000. Ten days after Zillow bought the home, the property went public for $ 505,900. When it didn’t sell, the company cut another $ 11,000 to $ 494,900.

According to DelPrete’s analysis, Zillow’s biggest competitor, Opendoor, continues to sell more homes than it buys, while home sales in Phoenix are declining. It also performs well in Atlanta, where Opendoor lists homes with a premium of 6.5% of the purchase price compared to Zillow’s 1.3% spread.

Zillow representatives declined to comment.

The company said on October 18th: It will stop making new offers to buy a home Reduce your share by 9.4% while processing the backlog. However, analysts most often shrugged off operational stumbling blocks and stocks recovered from these losses. The home flipping business dating back to 2018 is not yet profitable.

“Prices turned them on, they were a bit flatfoot, and probably a little too aggressive about bidding,” said Brad Ericsson, an analyst at RBC Capital Markets. “They probably don’t care so much. Making money isn’t that important at this stage of the game.”

Zillow and Opendoor are practicing a high-tech spin of home flipping called iBuying. Both companies use software-based algorithms to predict changes in home prices. They charge a fee instead of a typical real estate agent’s fee and pitch to their customers about the convenience of the service. Buying thousands of homes every quarter is a complex process and requires a lot of precision to do it right.

Rich Barton, CEO of Zillow, emphasizes that it is important to make competitive offers to reach the scale needed to make a profit in the business. He lamented in an August call with investors that soaring home prices have widened the spread between the cost of Zillow buying and repairing homes and the cost of selling real estate. rice field. As a result, the company, which purchased 3,800 units in the second quarter, has set a goal of purchasing 5,000 units a month by 2024 and is offering more offers.

“We saw a rapid increase in conversions throughout the quarter as we improved the strength of our offers,” he said.

Zillow and Opendoor are practicing a high-tech spin of home flipping called iBuying. Both companies use software-based algorithms to predict changes in home prices.

Richard Flor talked to a realtor this summer about listing a three-bedroom, three-bathroom rental for about $ 390,000 in the western suburbs of Phoenix, Tolleson, Arizona. Instead, he sold it to Zillow in September for about $ 412,000 and paid 1% of the service.

He then saw Zillow make a minor repair and relist the house for $ 387,000 two weeks later.

“I was wondering,’How do they make money,’” Flor said. “Maybe they know what I don’t know.”

Here’s why Zillow won’t be buying any more homes to renovate and resell this year

By JOE HERNANDEZ

10/20/2021

Al Bello/Getty Images

The real estate website Zillow announced it would stop buying and renovating homes through the end of the year as it works through a backlog of properties and it deals with worker and supply shortages.

“We’re operating within a labor- and supply-constrained economy inside a competitive real estate market, especially in the construction, renovation and closing spaces,” Jeremy Wacksman, Zillow’s chief operating officer, said in a statement.

“We have not been exempt from these market and capacity issues and we now have an operational backlog for renovations and closings,” he added.

Through its Zillow Offers program, the company buys homes directly from sellers, completes the necessary upgrades and lists them for sale. This lets sellers avoid having to do repairs or set up showings themselves, the company says.

Zillow, which is known for its online real estate listings, told shareholders that it purchased 3,805 homes through the program in the second quarter of this year, a major increase over previous years.

Zillow Offers, which launched in 2019, sold 2,086 homes and made a gross profit of $71 million over the same period.

The company announced on Monday that it wouldn’t sign any new contracts to buy homes through the end of 2021. Zillow said that it would still market and sell homes through the program and that it would also continue to buy houses with contracts that have already been signed but have yet to close.

The construction industry was one of many that were hit hard by the COVID-19 pandemic, which saw the cost of building materials soar. Meanwhile, the demand for homes — as well as their price tags — has surged.

While the astronomical prices of wood have decreased from their recent highs, other materials such as steel and piping remain costly or in short supply. On top of that, there is a serious shortage of construction workers.

Both the construction of new homes and the authorization of building permits fell in September compared with the previous month, according to the U.S. Census Bureau.

In an interview with Marketplace Morning Report last month, Associated Builders and Contractors economist Anirban Basu said the coronavirus was still causing problems in the housing industry. “The spread of the delta variant globally has increased supply chain issues. It means higher prices for inputs; it raises the cost of delivering construction services,” Basu said.

Zillow slams the brakes on home buying as it struggles to manage its backlog of inventory

By Anna Bahney, CNN Business

10/18/2021

Zillow will stop buying homes through Zillow Offers for the rest of the year, as the company’s iBuying program goes from full speed to full stop.

The company announced on Monday it would not contract to buy any more homes in 2021 in order to work through the backlog of homes it has already bought.

The “iBuyer” model used by Zillow and other real estate companies entails purchasing homes directly from sellers, and then re-listing the properties after doing minor work. But thanks to the current shortage on labor and materials, Zillow can’t close, renovate and resell the homes fast enough.

“We’re operating within a labor- and supply-constrained economy inside a competitive real estate market, especially in the construction, renovation and closing spaces,” said Jeremy Wacksman, Zillow’s chief operating officer, in a statement.

“Pausing new contracts will enable us to focus on sellers already under contract with us and our current home inventory,” said Wacksman.

Zillow will still market and sell the homes it has acquired through Zillow Offers, which has been on a purchasing tear this year. It bought 3,805 homes in the second quarter — a record high for the company and more than double the number of homes bought in the first quarter, according to a note to company shareholders.

Zillow, known for its online real estate listings, introduced an iBuyer program, Zillow Offers, in 2018 and now operates in 25 cities. Like other iBuyers — such as Opendoor, RedfinNow and Offerpad — Zillow Offers uses data and algorithms about the property and the market to make a cash offer on an off-market home, and buys directly from the homeowner.

IBuyers appeal to home sellers because closings can take place anywhere from 7 to 90 days after the contract is signed and can provide some certainty and control over the sale of their home without the hassle of finding an agent and prepping the house for market. According to Zillow, the fee to the seller for Zillow Offers averages 5%, but can vary based on market conditions.

Home purchases by iBuyers now account for about 1% of the market, according to a report from Zillow. The share is still a tiny part of the whole market, but shows tremendous growth over the past few years as the iBuyer share in some cities, like Phoenix, Atlanta or Charlotte, North Carolina, now tops 5%.

Zillow wasn’t alone among iBuyers in buying a lot of homes this year. IBuyers bought more houses, at higher prices, in the second quarter of this year than in any other quarter, according to research from Mike DelPrete, an independent real estate technology strategist and scholar in residence at the University of Colorado Boulder. That has surprised some skeptics who did not think the iBuyer model would be appealing to home sellers in a hot market.

His research suggests that sellers are drawn to the certainty and ease of iBuying and the market conditions fueled its growth.

Zillow’s move to halt purchases is surprising, he said, particularly because it is so sudden.

“iBuyers have access to a tremendous amount of data, they can see months into the future and plan their inventory,” said DelPrete. “So the fact that Zillow didn’t see this coming and wasn’t able to make adjustments before it had to resort to an iBuying lockdown is pretty surprising.”

This shift, he said, demonstrates how difficult this business model is to scale up. Large iBuyers need to be skilled at both managing billions of dollars in capital, but also the logistical specifics of prepping a home for sale, down to drywall and painting and closing deals.

“There is only so much that technology can do,” said DelPrete. “At the end of the day you need people to process a lot of transactions.”

However, the halt appears to be a Zillow-specific problem, not an iBuyer industry problem, DelPrete said.

“Zillow just kept barreling down and now they’ve hit this wall,” he said.

This is not the situation a growth-focused company wants to be in, he said.

“If you’re trying to be number one in the market, slamming on the brakes is one of the worst things you can do,” said DelPrete. “You want to make some adjustments before you get to that point — slow down, switch gears. This is not the preferred outcome for Zillow.”

Opendoor, the leading iBuyer ahead of Zillow at a distant second, said in a statement it is still open for business.

‘Insatiable demand’ for warehouse space continues in NJ

Rents surge to record high as developers scour state for booming logistics industry

By JON HURDLE

10/16/2021

Rents surged and vacancies dropped to a record low for warehouses and other industrial buildings in north and central New Jersey from June to September, a new report said Wednesday, as demand from e-commerce continued to fuel the state’s red-hot market for logistics space.

The asking price for industrial rents rose 15.6% to a record $10.72 per square foot while vacancies fell to 3.4% from 3.8% only three months earlier. For warehouses, which account for about three-quarters of the overall industrial market, the vacancy rate was even lower, at 2.9%, according to the report from Newmark, a commercial real estate company.

As in the first half of 2021, the growth was again driven by very strong demand from logistics companies for space to store and distribute an avalanche of goods ordered online.

“Insatiable demand from ecommerce, corresponding with a long-term shift in consumer spending habits towards online spending and away from traditional retail stores remains a key driver of leasing activity,” the report said.

Demand for logistics space has been strong for five years but was fueled further over the past year by online shopping during the pandemic. It has also been driven by the state’s proximity to Port Newark-Elizabeth where one of the nation’s largest volumes of consumer imports enters the country, and by New Jersey’s position at the heart of the populous Northeast market.

While the boom has created thousands of jobs, including some 50,000 at Amazon alone, it has also sparked protests and lawsuits in some communities where residents fear that local roads will be choked by new truck traffic, and that remaining rural enclaves will be occupied by giant warehouses that may cover a million square feet or more.

In the Legislature, public concern that warehouses affect areas beyond the towns where they are built has also spawned a bill co-sponsored by Senate President Steve Sweeney (D-Gloucester) that would require towns facing a warehouse application to alert neighboring municipalities and try to win their support for the project.

Numbers show big-time growth

The new data shows the boom is only accelerating. Industrial space under construction, almost all of which was for warehouses, rose to 13.9 million square feet in the latest quarter from 13.4 million in the second quarter of 2021. Despite a supply shortage, the amount of industrial space leased in the first three quarters of this year, 28 million square feet, exceeded that for all of 2020.

In another key indicator of the strength of demand, net absorption — the difference between the amount of industrial property that became occupied during the quarter, and that which became vacant — jumped to 4.7 million square feet in the latest quarter from 3.1 million square feet in the previous three months.

“It’s remarkable to me that it keeps going up,” said Tim Evans, director of research at New Jersey Future, a nonprofit that advocates for “smart growth.” He said the warehouse boom can’t be fully explained by the surge in online shopping during the pandemic, and may have also been fueled by an increase in the volume of imported goods arriving at Port Newark-Elizabeth from Asia since the Panama Canal was widened to accommodate bigger ships in 2016.

Evans predicted that the continued high demand for warehouse space will result in both vacant and previously developed land being obtained for an industry that wants to be as close to the port as it can. That process may involve “second-generation” redevelopment of sites that first held factories, then became office parks, and would now be occupied by warehouses.

“As factories close to the port get used up, they might start buying second-generation redevelopment sites like office parks,” he said.

The report said there’s a “widening imbalance” between supply and demand, especially in sub-markets where available land is limited. They include the Meadowlands, where rents jumped 28.5% in the latest quarter compared with a year earlier. The report predicted that the sharply higher rents there will spur developers to redevelop land or reuse existing buildings.

Major transactions included 840,000 square feet leased to Peloton, the fitness equipment maker, at Linden; 511,000 square feet in Warren County to Alan Ritchey, a logistics provider, and 326,000 square feet in the Meadowlands taken by TJ Maxx, a clothing retailer.

In the warehouse sector specifically, the highest asking rent among 21 local markets was $14.73 per square foot in the Meadowlands, followed by $14 in the market around New Jersey Turnpike Exit 12 where the vacancy rate was virtually nonexistent at 0.1%.

No end in sight

There’s no sign that high rents and low vacancy rates will let up any time soon, given continuing high demand from logistics companies, the report said. It forecast that developers will continue to encounter rising construction costs, shipping delays and labor shortages.

“In the coming months, robust demand from ecommerce and logistics companies is expected to maintain a record low vacancy rate, driving further growth in warehouse rents,” it said.

Micah Rasmussen, a Rider University professor who led a successful campaign against a planned warehouse in Upper Freehold earlier this year, said people should consider whether New Jersey is getting over-developed — in light of the ongoing warehouse boom and the devastating flooding caused by Tropical Storm Ida.

“I think the shortcomings of our over-development became much clearer to a lot of people during Ida,” he said. “We need to rethink what we’re doing, and given what’s happening in the market, it seems like the perfect time for us to do that.”

In N.J., the fall housing market is starting to look better for buyers

BY ALICIA SMITH

10/08/2021

The red hot residential real estate market is beginning to cool slightly, and this trend is expected to continue for the remainder of the year.

Low interest rates, low inventory, and buyers looking to leave urban areas, such as New York City, for more space in the suburbs, were largely driven by cheap interest rate rates and low stock levels in New Jersey City.

However, according to Jeffrey Otteau, a real estate economist and president of the Otteaux Group, the home buying demand is running at slowed pace in New Jersey four months later.

He explained that Its not that it’s collapsing, he said. It’s normalizing.

According to Otteau’s data, contract sales were down statewide by 12 percent in June, 22 percent on July, 16 percent, and 22 cents in August for the first three weeks of September.

Sales are lowering, according to him, because home prices have risen so much that they are unaffordable even with low interest rates. And urban flight in the middle of the epidemic, which brought city-dwellers who wanted more room to the suburbs, has ended.

Migration from the city to the suburbs is now reversing as cities renown, Otteau said. As employers are advising workers to return to the office, were starting to see housing shift back in toward the city.

According to Otteau’s data, contract sales in Hudson County have risen by 35% every year to date, according to him.

And according to New Jersey Realtors August report, closed sales in Hudson County were up 17.1% in August alone, despite closed doors falling by 10% statewide.

Irene Barnaby of Compass in downtown Jersey City said she’s seeing buyers who were renting in the area and want to profit from low interest rates, international buyers, and some of the situations when people who fled Hudson County” traffic now want back.

One couple she worked with sold their three-bedroom apartment in downtown Jersey City and moved to Maplewood in May 2020. They called her about 6 months ago and stated they sold their Maplewood house and were returning to Jersey City.

They missed the vibrancy and being in the center of the action, and having access to New York City, Barnaby stated.

People who are buying in Hudson County still want space, she added. The majority of people are searching for two or more bedrooms and want some sort of outdoor space. She said, “One-bedrooms are difficult to sell,” and she remarked.

Another factor slowing home sales overall is that home prices rose 12% in 2020 and are on the verge of risen 17 percent this year, according to Otteau, stating that prices grew an average of about 3% for each of the previous 7 years.

House prices can only rise as fast as salaries, he said. Banks won’t lend buyers enough money to afford a house after ten years of that (faster than salary growth). There must be a correction to follow, if home prices rise faster than salaries.

Otteau predicts a price increase of 5% in 2022 and regress of 5 percent in the 2023.

However, he said, it’s still a good moment to purchase. He explained, “You’re going to get a lower interest rate now than in the future,” he added.

According to Reuters, American Federal Reserve policymakers may be able to raise interest rates next year.

According to Otteau’s statistics, the highest segment of the housing market is homes in the $1 million to $2.5 million sales range, which is responsible for approximately 45 percent of sales, followed by the $600,000 to $1 millions sales spectrum, with 30 percent sales.

Those buyers are chasing up and, in the process of purchasing, they’re also increasing the inventory of homes on the market because they sell their existing homes.

People were concerned about job security, so they didn’t want to take on a larger mortgage, Otteau said, because trade-up buyers were not selling last year. They were concerned that strangers gathered across their houses in the middle of a health crisis.

However, the trade-up market hasn’t completely exploded.

Missy Iemmello, office manager for Weichert Realtors in Morris Plains, whose 120 agents work in the Morris, Sussex, Warren, Bergen, and Essex counties, said in September that she saw a rise in inventory that quickly slowed.

We were all delighted. We believed they’ve been anticipating this year, Iemmello added. Then it was simply a short blimp, all of oh, this was subsequently merely en route to victory.

Hurricane Ida, according to Iemmello, stopped the trend.

People got water where they never had water before, she explained. I believe we should see inventory numbers increase in the following weeks.

Frustrated House Hunters Are Giving up on Buying Only to Face an Expensive Rental Market

By Aly J. Yale

9/22/2021

Cramped in a one-bedroom, new parents Kristina and David Mahon were desperate to buy a larger home. But after scouring the Pompano Beach, Florida market for nearly a year (and losing out on 20 houses in the process), the pair eventually gave up.

Now, the couple — with a 10-month old baby in tow, no less — are renting, a decision Kristina says they felt “forced” into.

“I feel like I’m wasting money for something that’s not mine,” Kristina says. The rental“options were very limited, and the prices were on the high side of what we were comfortable spending on a rental.”

The Mahons’ is a common storyline these days, according to those in the industry. Burned-out house hunters are tired of bidding wars, rising prices and dwindling options and are bowing out of the purchase market, opting to rent instead.

“It’s common given the current market and environment that we are in,” says Kaley Tuning, the Native Realty agent who worked with the Mahons. “It just becomes frustrating for the everyday buyer. I’ve had buyers bid upwards of $40,000 over asking price and still get outbid.”

Unfortunately, the pivot to renting isn’t always easy. While the move may afford frustrated buyers time to wait out the competitive housing market, it often means entering an equally hot rental scene — one where rising rents and dwindling supply are growing concerns.

According to Realtor.com, median national rents grew a whopping 11.5% between August 2020 and August 2021. And rent applications? Those are up as much as 95% in some cities, according to apartment listing platform RentCafe.

For hopeful homeowners, it’s made for a unique catch-22 that’s as frustrating as it is costly.

Rents are on the rise

It’s no secret the housing market’s been hot this year. The purchase market has boomed in nearly every corner of the nation since last spring. Home prices are up 17% over the year, and inventory, while improving, is still near record lows.

The rental picture has been more mixed, though. At the start of the pandemic, vacancies in big cities rose and prices dropped, while demand for suburban rentals skyrocketed. Now, rents are bouncing back across the country, reaching well above pre-pandemic levels in many areas.

According to Realtor.com, the typical rent now clocks in at $1,633 per month — $169 more than this time last year and almost $200 more than 2019’s numbers. And in nearly half of the country’s biggest cities? Monthly starter home payments are more affordable than average rents.

The hot housing market has a lot to do with this spike in rent costs. With rising home prices and limited for-sale listings, more and more buyers are stepping back. This puts pressure on rental inventory and drives up rents.

As Lisa Harris, an agent at RE/MAX Center in Braselton, Georgia, explains, “Fewer homes listed for sale and much higher prices for them have kept many want-to-be buyers in their rental units, taxing the rental supply.”

The pandemic plays a role, too. Eviction bans have kept many non-paying renters in place, tying up units for much of the last year. While the CDC’s eviction moratorium was shot down late last month, the experience has made many landlords warier than ever.

“Not only have the prices increased, but the demand on tenant screening seems to be getting much more stringent,” Harris says. “Landlords are seeking tenants with higher credit scores, higher deposits, no pets, a clean criminal history and more.”

The trickle-down of higher rents

Alex Lashner, like the Mahons, has experienced the difficult rental market firsthand. She even had to expand her rental search to account for price increases and is now looking as far as 90 minutes from her office just to stay on budget.

“I’m hoping it will be a short-term sacrifice so I can buy closer to my workplace a few years down the line,” she says.

Lashner was originally looking to buy her first home somewhere in Bucks County, Pennsylvania, but due to the competitiveness of the market — and her refusal to waive contingencies or overpay (as many buyers are forced to do lately), she lost out on every property she bid on. She finally opted to rent, only to find rising prices there, too.

“I’m frustrated that buying a three-bedroom home in my budget is cheaper than renting when you compare the monthly costs of a mortgage, property taxes and HOA fees versus the rental costs for a two-bedroom or even a one-bedroom apartment,” Lashner says. “That’s where my real sticker shock is.”

Rising rents are more than just a budgetary strain for hopeful buyers, though. They also make it harder to save, which could push back those homebuying goals even further. The Mahons are one household in that camp, something Kristina calls “frustrating.”

“Instead of us paying down our own mortgage and building equity, we are paying someone else’s mortgage,” she says. “For the next year or as long as we are renting, we will not be able to save as much as we had hoped.”

Buyers who are forced to sign long-term leases have another dilemma, too: What if mortgage rates go up?

Interest rates have been hovering near historic lows for months now and have played a major role in boosting buyer demand. Kristi Nowrouzi, a mortgage loan officer with Geneva Financial, says many buyers who have backed out of the market recently are concerned those conditions could change.

“There’s a fear of missing out on the low-interest-rate environment,” Nowrouzi says. “Inflation is blowing up and who knows what rates will look like next year at the end of an annual lease agreement.”

What’s the solution?

One option for buyers facing sky-high rents is to opt for a month-to-month lease. The flexibility usually comes with a slightly higher monthly rent, but it ensures you can act quickly should the right house hit the market.

“By doing a month-to-month lease, even though rent might be slightly higher than signing a long-term lease, they can be ready to take action,” says Shmuel Shayowitz, president and chief lending officer at Approved Funding, a mortgage lender in New Jersey. “They can also continue to actively look for homes and, even if pricing doesn’t soften, be in a better position to act.”

Fortunately, strategies like this might not be necessary for long. Buyers still face plenty of challenges, but recent data points to growing housing supply — particularly in the starter home segment. Existing home sales have also slowed, falling 2% in August, and price growth has decelerated as well. According to Realtor.com, 17% of all listings had price reductions in August.

“The market is absolutely shifting now, and prices are decreasing a bit and sellers aren’t getting as high price per square feet as they were a few months ago,” Nowrouzi says.

A completely cooled-off market, though? That could be a long way in the future. Until then, Tuning says, “Patience is a virtue.”

为解住严重宅荒 美联邦政府要盖10万户平价宅

来源:经济日报

9/02/2021

在美国房价持续高涨之际,白宫官员表示,美国政府为纾解严重住宅荒,将采取一系列立即可实施的步骤,以现有经费和权力,在未来三年兴建、销售10万户平价住宅。

路透引述官员说法报导,这套计划最快1日宣布,将聚焦于扩大对个人和非营利机构销售房屋,同时对大型投资人买房设限。第2季全美各地每售出六户住宅,就有一户被投资大户买走。

美国房屋需求在新冠肺炎疫情爆发初期激增,反映民众为居家办公和学习购置更宽敞的房子。但待售屋不足和供应链瓶颈把房价推得更高,租金行情跟着水涨船高,加重家庭财务负担。白宫官员说,全美平价住宅估计短缺多达400万户。

白宫官员表示,美国总统拜登(专题)已提议,斥资逾3,000亿美元增建200万户平价住宅,这项措施是3.5兆美元基础建设投资案的一部分,正在国会审议中。但拜登希望推动立即可行步骤。

这套新计划将涵盖乡村与都会地区的住宅建案,重点摆在平价房市,希望能协助房屋自有率偏低的有色人种族群。

此计划将由美国住宅与都市发展部(HUB)部长法吉(Marcia Fudge)宣布,具体行动由该部、财政部及房贷机构房利美(Fannie Mae)与房地美(Freddie Mae)等联邦监管机构共同规划。“两房”合计占全美11兆美元房贷市场的一半。其中,一大关键步骤是重启曾由财政部与HUB合办但在2019年结束的“风险分摊计划”,该计划让各州住宅金融机构能扩大提供低利贷款,促进兴建平价住宅。

此计划也将提高组合屋及二至四户多户型不动产的供应量,希望透过房地美扩大融资达成目标。同时也将采取行动,限制对大型投资人销售一些由联邦住宅管理局(FHA)提供担保的不动产。

拜登政府另打算与各州和地方政府合作运用现有联邦资金,并协助减少排他性分区(exclusionary zoning)等阻挠提高住宅供应量的做法。

White House tackles housing shortage with plan for 100,000 affordable homes

By Andrea Shalal

9/02/2021

WASHINGTON, Aug 31 (Reuters) – The Biden administration is taking steps to address a severe housing shortage in the United States by creating and selling 100,000 affordable homes over the next three years using existing funds, the White House said on Wednesday.

The moves will focus on boosting home sales to individuals and non-profit organizations, while limiting sales to large investors, who scooped up one in six homes sold in the second quarter, according to a White House statement.

Demand for housing soared early in the pandemic as Americans sought more spacious accommodations for home offices and home schooling, but a shortage of homes for sale and supply chain bottlenecks have driven housing prices sharply higher.

Rental prices, which typically follow the lead of house prices, are also a big concern, given that even before the pandemic 11 million families – or nearly a quarter of all renters – were already spending more than half their income on rent, according to the White House.

The United States has an estimated shortage of as many as 4 million affordable housing units, White House officials say.

U.S. President Joe Biden has proposed spending over $300 billion to add 2 million more affordable housing units as part of a $3.5 trillion investment package being considered by Congress, but wanted to push forward with immediate steps that could be taken now, the White House said.

The plans will cover rural and urban housing projects, with a focus on aiding communities of color, where home ownership rates have lagged historically.

U.S. Housing and Urban Development (HUD) Secretary Marcia Fudge will announce the measures after touring a new five-story affordable housing complex in Philadelphia on Wednesday.

Fudge called the initiatives “significant downpayment” on Biden’s commitment to boost the supply of affordable rental housing, expanding access to capital for state Housing Finance Agencies, empowering local communities to build more affordable housing and promoting equitable housing policies.

Specific actions are planned by Fudge’s department, the U.S. Treasury and agencies such as Fannie Mae and Freddie Mac, which will increase financing opportunities to enable more Americans to purchase homes, the White House said.

One key step is the revival of a joint Treasury-HUD “Risk Sharing Program” that ended in 2019 and that will enable state housing financing agencies to provide more low-cost capital for affordable housing development.

The plans will also boost the supply of manufactured housing and 2-4 unit properties by expanding financing through Freddie Mac, while taking steps to limit the sale of some U.S. Federal Housing Administration-insured properties to large investors.

Investor purchases, which have been as high as one in every four homes in some communities, have driven up prices for lower-cost houses and triggered fierce competition for starter homes, the White House said.

The administration also plans to work with state and local governments to leverage existing federal funds, and help reduce exclusionary zoning and other practices that have discouraged efforts to boost the supply of housing, the official said.

The Federal Housing Finance Agency “will begin to study the interaction between exclusionary zoning and our regulated entities,” said acting Director Sandra L. Thompson.

如何计算一个投资房产的租金回报率?

By Willy Rong

3/07/2021

一直以来都有人问我,如何计算一个投资房产的租金回报率?我答过,但总是似是而非。

今天就这个问题给出我的计算公式Return Of Investment (ROI),仅供大家参考。

这个问题要从两方面讨论,看你是全额现金买房?还是贷款80% 买房?

(全额现金买投资房产)租金回报率 = (12月的租金 – 一年的各种花费)/ 买房价

(贷款80%买投资房产)租金回报率 = (12月的租金 – 一年的各种花费和贷款 )/ (

20%首付+ Closing Cost )

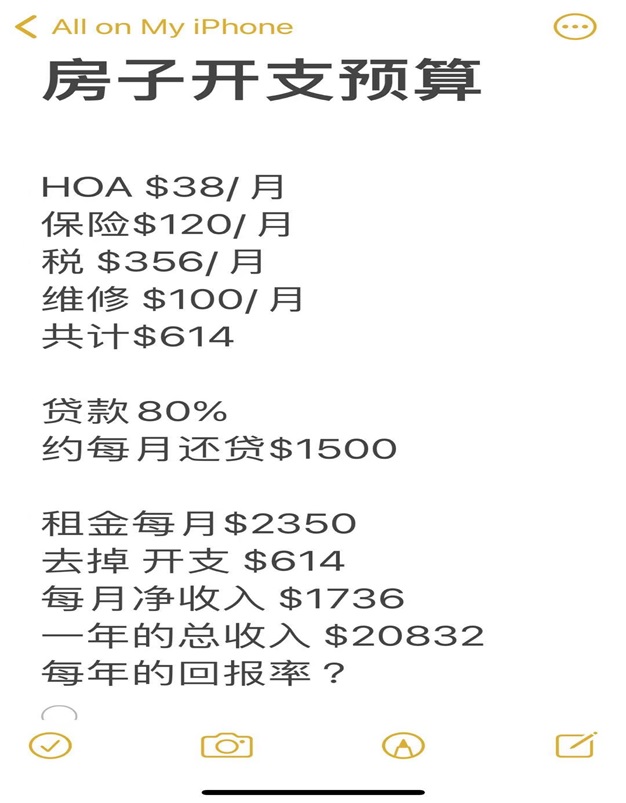

我们还是以一个$38万美元买房实例来计算,比较直观:

房子开支预算:

HOA $38/月; 保险 $120/月; 税 $356/月; 维修 $100/月。

共计 $614。

贷款 80%, 约每月还贷$1500;

租金每月$2350;去掉开支 $614; 每月净收入 $1736;

一年的总收入 $20832。

问:一个$38万美元的房产,每年的回报率?

(全额现金买投资房产)租金回报率 = (12月的租金 – 一年的各种花费)/ 买房价

$38万美元房子的租金回报率 = 一年的总收入 $20832 / 买房价$380,000 = $0.0548

全额现金$38万美元房子的租金回报率一年约为:5.5%;

(贷款80%买投资房产)租金回报率 = (12月的租金 – 一年的各种花费和贷款 ) / (

20%买房首付 + Closing Cost)

$38万美元贷款80%房子的租金回报率 = (一年的总收入$20832 – $18000) / (首付 $

76000 + $5000 Closing Cost ) = $0.0349

$38万美元贷款80%买投资房产的租金回报率一年约为:3.5%.

这个$38万美元的房子在最好学区,房子升值潜力大!

考虑到加上房子产权equity 上涨的因素,一年在6%-8%。所以要加上一个Equity 增值

率,换句话说,是用$81000 买了一个$38万美元的房产,是用杠杆买的房子。

这里有2个概念:一个是租金回报率;一个是Equity 回报率;

利用杠杆买房,就要让银行在这个房子上也赚一些钱,所以贷款租金回报率3.5%.要低

于全额现金租金回报率5.5%,这个逻辑是对的,那个2% 回报率的差让银行赚去了。

什么是智慧?智慧就是解决问题的能力!

能够把一个复杂问题简单化,用直白的方式讲清楚,这也是智慧。

现在亚特兰大地区(佐治亚),一个房子的租金回报率大概在3% ~ 6%左右,真心话,

投资房净租金回报率6%是一个不错的回报。

你若嫌上面二手房一年的租金回报率还低,你可以全现金买126包租5年的项目,一年的

租金回报率为净6%。

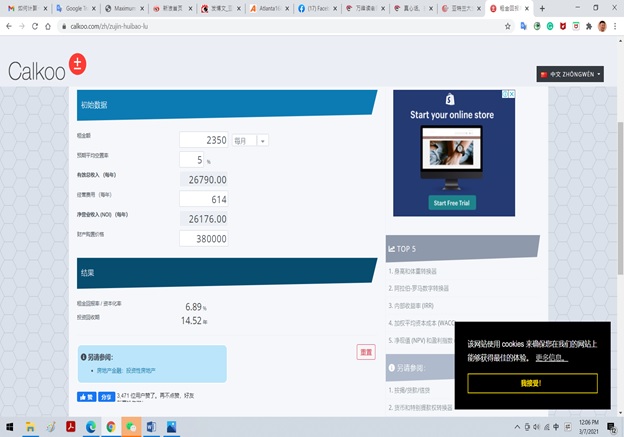

下面是在网上找到的租金回报率计算器,大家可以去练习:

租金回报率

https://www.calkoo.com/zh/zujin-huibao-lu

提示:算大账不算小账,可能公式不够严谨,但逻辑是对的。

Source: http://www.mitbbs.com/article_t/Georgia/31320547.html

Six Spaces Home Staging

Contact: Hongliang Zhang

Tel: 571-474-8885

Email: zhl19740122@gmail.com