Six Spaces Home Staging

Contact: Hongliang Zhang

Tel: 571-474-8885

Email: zhl19740122@gmail.com

浅论房屋出售前Home Staging的益处

第四章

10/12/2021

接上篇:

三、做家具布置前后的效果分别,结合案列照片讲解Staging的优势所在

统计显示,经过装饰后的房屋比未经装饰的出售速度高出2-3倍,价格也高出11%。 根据北美房地产售前美化协会(RESA, Real Estate Staging Association)的调研报告显示,买家往往是在看到房子的前30至40秒就决定了要不要这个房子的。「这是北美非常权威的机构的统计数字。所以我们同时鼓励大家自己动手装饰自己的房子,有时候如果本人在房屋出售前住在家里,其实就是天然的Staging,合理专业的Staging开销将会远远将低于你布置后所产生的价值,这也是为什么如今越来越多的人关注到这个步骤,也投入更多的时间和精力去做售前布置。但如果房子在出售前全部是空的,而且是年久未装修的,强烈建议要做专业的家具布置,因为专业人士会了解不同房屋突出的重点,运用色彩、装饰、布局来让整个房屋提升品质,并巧妙隐藏房屋内部结构的缺陷。请记住,售房时您的家即将成为别人的家,要用别人的眼光来布置自己的家,去除那些显示自己个性和习性、宗教、文化、信仰的装饰,收起您的照片和私人物品,让您的家符合更多人的口味。泛泛的说了这么多,那么Staging中细节上可以做那些工作呢?加入什么元素才能更受买家欢迎呢?前后差别真的像上文所叙述的那样差很多吗?我们结合图片会更清晰。

1、突显空间多样性

您的房屋格局设计会给买家一个心理暗示,让他也会融入您的格局分配来观察房间布局及实用性。在布置房屋内部结构时,如果能赋予该房间多个实用功能,会让买家眼前一亮,也会让他产生更多遐想。小户型比如Condo公寓中多样性的表现最为突出,让一个Den身兼Office和Guest Room、书房内摆设一张符合风格的沙发床创造了额外的睡眠空间都是很好的例子。只要发挥一下创造力,变化出不同空间区域功能都会增色不少。

2、Home Staging有大不同

Home Staging中文称房屋预售前布展,俗話说的好「人靠衣裳马靠鞍」,屋子預售前也需要好好收拾一番。 Home Staging可不仅仅是简单的清洁房屋,摆正家具,而是结合了房屋销售和室內设计的概念,让房屋在短期内涣然一新,极大的凸显房屋的优点,扬长避短。如今市場上待售屋中, 几乎都做Staging, 原因在於有 Staging的房子比沒有做的的要更快售出 (全國平均值是31.8天 vs. 161天), 而且卖价更高 (投資報酬率是 343%), 而有91% 的Agent会建议屋主投資一点钱將房子 Staging,staging是在营造一种气氛。就像去相亲,女孩子都要化妆,其实和staging是一样的。这体现了我们对工作以及卖家尊重的程度。如果为潜在买家呈现的是空房子,很难让他们想像在这个空间中可以做什么,或在那个空间里可以放什么搭配。如果能摆上一些家具,就有了很好的画面感。或者卖家本身就住在房子里,那就是一种天然的staging。我们这样做的目的是为了给买家一种实际的感官。相对来说staging过的房子肯定比什么都不放、没有任何感觉的空屋出售速度和价格都会有非常大的提升。

3、Home Staging是一种投资

社区中许多有人觉得staging的花费很贵。Staging是一种比较先进的东西。从国内过来的移民会觉得这样做比较虚,因为摆完了就没有了,就是这几天的使用权。有些人买了一、两百万的好房子,大几千的好家具不捨得买,也是大有人在的。不捨得花钱staging的人有很多,因为他们看不到这种意识形态。和拥有先进一点的思想的人或者本地人相比,移民的确对staging的意识会不太一样。因为他们认为经济利益会达不到。,如果大家能反方向去思考staging把它看成是一种投资(investment),而不是开销(cost),就会好一些。这和大家租车一样。如果花了几百块租车出去玩几天,租车费就是花费。但如果这几天你租了车去顺路拉了几个客人赚了钱,那这几百块就是投资。看事物的角度不一样。Staging如果以投资的角度看,假如花费三千元,房子可以卖得更快,也可能卖得更多,这就是投资。staging对卖家来说是个投资。房子没有卖掉,每个月都要交月供(mortgage payment),通常大家的房子每个月都有几千的开销,其实和staging每个月续租金是一样的。Staging如果能缩短卖房子的时间值,卖家其实是省钱的。尤其是已经买了房子的那些屋主,还要同时顾及现有房子的贷款的人,卖得快更是等同于赚了。 虽然staging好处多,但它其实只是辅助作用。不一定摆了东西就可以卖得更快和更多。现在的市场和两三年前不一样,Staging可以做,但是不能因此就把房子的价格定得过高。价格不合理,做staging也没用。花很多钱进去,但如果是想要卖到更高一个level(层级)的价格,就需要简单的装修和Staging双管齐下碰撞出火花,一定能够起到非常好的销售效果!卖房,价格是最主要的东西之一。总之在价格可控的范围内,能做到最好的staging,就像新娘出嫁之前的化妆一样,是必不可少而且是非常好的投资生意!

4. Home Staging的经济账

一些卖家在卖房前常常会问,需要为房子做何种程度的装修,以及预算应控制在多少为好?对此表示:如果预算在1000元内能办成的装修,那就去做;如果预算在1到3万之间,要考虑一下性价比;如果预算超过3万,就不大必要,要选择该做的去做。什么是该做的?比如刷墙、换电器、柜面、卫生间换一下马桶等,当然也要根据每一个房子具体的状况分析。Staging在这样的旧房子其实是有效果的。在定价合理的基础上,更要用心的去做staging。因为如果房子位于老区,竞争者一定也是较为老旧的房子。所以如果你做了staging,别的卖家没有,在网络上展出的时候,无论细节以及布展产生的美感,一定会起到事半功倍的效果。另外过分的装修,比如地板花了两万块,但是颜色或者材料,新买家不喜欢,就会造成一个尴尬的局面。买家会拿这个和卖家去还价,因为觉得这个东西没有必要存在,或者搬进去之后还要换掉。所以我觉得在卖房之前花大手笔做过分的装修,其实没有太大的必要,一旦颜色以及风格原则不合适,会容易让买家造成不喜欢的感觉。除非你是真的花10万以上的大价钱,找最好的装修公司去做大翻修。在做staging的过程中,的确旧房子要注意不要使用过度高档奢华的装饰品和家具,因为用了不会加分,反倒把房子给拉低了,让客户感觉家的美是一种非常的不平衡的美,就像在故意掩饰什么缺点。这种房子布展要着重在色调上,让它产生有一种家的温馨感觉,空间感很舒服。如果可以再加一点点特色。就会使一个成功的案列了,这个是我们对旧房子的策略。如果是豪宅和高端住宅,则必须选择相对高级的装饰品和傢俱,以搭配房子本身的气质。

这些年的确在工作的过程中也见到了过度装修和过度staging的房子。「一个小区,如果均价在100万,不装修都可以卖90万,但你花了十几万去装修,最后卖了102万,那麽其实回报率不高,还不如不特别大动,做一些小修小补, 以及配合staging做出最好的效果。比如卫生间,尽量干净整洁,物件有好的工作状态, 不需过分装修。如果你打算在自己的房子里住很久,每年阶段性的装修升级花个五千到一万,我觉得很好,毕竟是自己享受。另外,过分装修会让买家造成一种恐惧感。我之前有个买家看到过度装修的房子,会想屋主是不是在掩饰什么?之前发生过什么事情或者事故? 过度staging的我也见过,非常奢华,让人进去一看就喜欢。但是花了太多钱投资进去,最后价格也没有卖多么好。

是不是过度的staging, 很多时候要看每个人的风格。我认为过度是,比如这个客厅空间感很好,但过度配置了很全和大的家具,就会适得其反,要知道,做布展最好的效果是合理范围内使用最小的家具展示最大的空间,同时,我个人会避免同一个房间出现同样的东西。比如很多房子是开放式格局,客厅和餐厅是在一起的,装饰品要尽量避免重复,也不宜过多。总之布展房屋的空间并不是家具多,档次越高就越好,是用最精确最适合的饰品去展示最大的空间美感!

未完待续。。 。

Tel: 551-580-4856 | Email: F.WINNIE.S@GMAIL.COM

诚招美国和加拿大法律服务代理

因公司发展需要,诚招美国和加拿大法律服务代理。

要求:

懂英语、或西班牙语、或法语。

能合法工作有社安号或工号。

无需改行, 可以兼职。

大学生和有销售经验优先考虑。

自雇生意公司发美国报税1099,加拿大T4A

有意了解详情, 请扫码加微信, 非诚勿扰!

如何计算一个投资房产的租金回报率?

By Willy Rong

3/07/2021

一直以来都有人问我,如何计算一个投资房产的租金回报率?我答过,但总是似是而非。

今天就这个问题给出我的计算公式Return Of Investment (ROI),仅供大家参考。

这个问题要从两方面讨论,看你是全额现金买房?还是贷款80% 买房?

(全额现金买投资房产)租金回报率 = (12月的租金 – 一年的各种花费)/ 买房价

(贷款80%买投资房产)租金回报率 = (12月的租金 – 一年的各种花费和贷款 )/ (

20%首付+ Closing Cost )

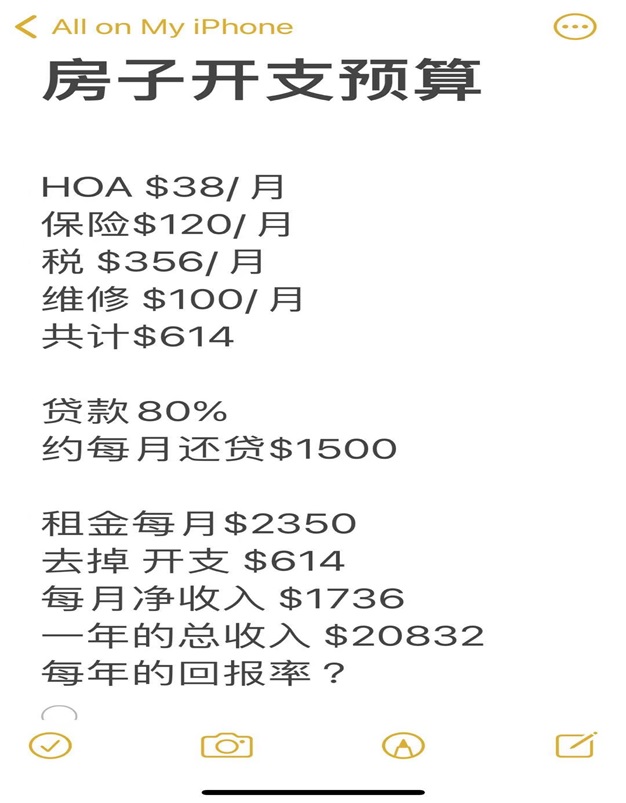

我们还是以一个$38万美元买房实例来计算,比较直观:

房子开支预算:

HOA $38/月; 保险 $120/月; 税 $356/月; 维修 $100/月。

共计 $614。

贷款 80%, 约每月还贷$1500;

租金每月$2350;去掉开支 $614; 每月净收入 $1736;

一年的总收入 $20832。

问:一个$38万美元的房产,每年的回报率?

(全额现金买投资房产)租金回报率 = (12月的租金 – 一年的各种花费)/ 买房价

$38万美元房子的租金回报率 = 一年的总收入 $20832 / 买房价$380,000 = $0.0548

全额现金$38万美元房子的租金回报率一年约为:5.5%;

(贷款80%买投资房产)租金回报率 = (12月的租金 – 一年的各种花费和贷款 ) / (

20%买房首付 + Closing Cost)

$38万美元贷款80%房子的租金回报率 = (一年的总收入$20832 – $18000) / (首付 $

76000 + $5000 Closing Cost ) = $0.0349

$38万美元贷款80%买投资房产的租金回报率一年约为:3.5%.

这个$38万美元的房子在最好学区,房子升值潜力大!

考虑到加上房子产权equity 上涨的因素,一年在6%-8%。所以要加上一个Equity 增值

率,换句话说,是用$81000 买了一个$38万美元的房产,是用杠杆买的房子。

这里有2个概念:一个是租金回报率;一个是Equity 回报率;

利用杠杆买房,就要让银行在这个房子上也赚一些钱,所以贷款租金回报率3.5%.要低

于全额现金租金回报率5.5%,这个逻辑是对的,那个2% 回报率的差让银行赚去了。

什么是智慧?智慧就是解决问题的能力!

能够把一个复杂问题简单化,用直白的方式讲清楚,这也是智慧。

现在亚特兰大地区(佐治亚),一个房子的租金回报率大概在3% ~ 6%左右,真心话,

投资房净租金回报率6%是一个不错的回报。

你若嫌上面二手房一年的租金回报率还低,你可以全现金买126包租5年的项目,一年的

租金回报率为净6%。

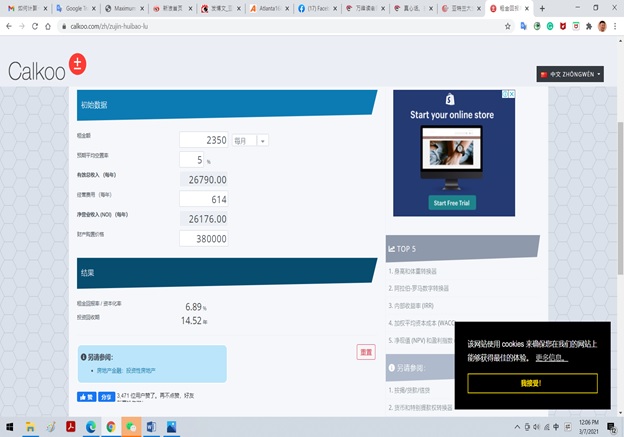

下面是在网上找到的租金回报率计算器,大家可以去练习:

租金回报率

https://www.calkoo.com/zh/zujin-huibao-lu

提示:算大账不算小账,可能公式不够严谨,但逻辑是对的。

Source: http://www.mitbbs.com/article_t/Georgia/31320547.html

How to Calculate ROI on a Rental Property

Why it’s important to know a property’s ROI before buying real estate

By JEAN FOLGER

3/07/2021

One of the main reasons people invest is to increase their wealth. Although the motivations may differ between investors—some may want money for retirement, others may choose to sock away money for other life events like having a baby or for a wedding—making money is usually the basis of all investments. And it doesn’t matter where you put your money, whether it goes into the stock market, the bond market, or real estate. https://66fb8f8f96c41eb6be84c3a0428532d2.safeframe.googlesyndication.com/safeframe/1-0-37/html/container.html

Real estate is tangible property that’s made up of land, and generally includes any structures or resources found on that land. Investment properties are one example of a real estate investment. People usually purchase investment properties with the intent of making money through rental income. Some people buy investment properties with the intent of selling them after a short time.

Regardless of the intention, for investors who diversify their investment portfolio with real estate, it’s important to measure return on investment (ROI) to determine a property’s profitability. Here’s a quick look at ROI, how to calculate it for your rental property, and why it’s important that you know a property’s ROI before you make a real estate purchase.

KEY TAKEAWAYS

- Return on investment (ROI) measures how much money, or profit, is made on an investment as a percentage of the cost of that investment.

- To calculate the percentage ROI for a cash purchase, take the net profit or net gain on the investment and divide it by the original cost.

- If you have a mortgage, you’ll need to factor in your downpayment and mortgage payment.

- Other variables can affect your ROI including repair and maintenance costs, as well as your regular expenses.

What Is Return on Investment (ROI)?

Return on investment measures how much money, or profit, is made on an investment as a percentage of the cost of that investment. It shows how effectively and efficiently investment dollars are being used to generate profits. Knowing ROI allows investors to assess whether putting money into a particular investment is a wise choice or not.

ROI can be used for any investment—stocks, bonds, a savings account, and a piece of real estate. Calculating a meaningful ROI for a residential property can be challenging because calculations can be easily manipulated—certain variables can be included or excluded in the calculation. It can become especially difficult when investors have the option of paying cash or taking out a mortgage on the property.

Here, we’ll review two examples for calculating ROI on residential rental property: a cash purchase and one that’s financed with a mortgage.

The Formula for ROI

To calculate the profit or gain on any investment, first take the total return on the investment and subtract the original cost of the investment.

Because ROI is a profitability ratio, the profit is represented in percentage terms.

To calculate the percentage ROI, we take the net profit, or net gain, on the investment and divide it by the original cost.

For instance, if you buy ABC stock for $1,000 and sell it two years later for $1,600, the net profit is $600 ($1,600 – $1,000). ROI on the stock is 60% [$600 (net profit) ÷ $1,000 (cost) = 0.60].

Calculating ROI on Rental Properties

The above equation seems simple enough, but keep in mind that there are a number of variables that come into play with real estate that can affect ROI numbers. These include repair and maintenance expenses, and methods of figuring leverage—the amount of money borrowed with interest to make the initial investment. Of course, financing terms can greatly affect the overall cost of the investment.

ROI for Cash Transactions

Calculating a property’s ROI is fairly straightforward if you buy a property with cash. Here’s an example of a rental property purchased with cash:

- You paid $100,000 in cash for the rental property.

- The closing costs were $1,000 and remodeling costs totaled $9,000, bringing your total investment to $110,000 for the property.

- You collected $1,000 in rent every month.

A year later:

- You earned $12,000 in rental income for those 12 months.

- Expenses including the water bill, property taxes, and insurance, totaled $2,400 for the year. or $200 per month.

- Your annual return was $9,600 ($12,000 – $2,400).

To calculate the property’s ROI:

- Divide the annual return ($9,600) by the amount of the total investment, or $110,000.

- ROI = $9,600 ÷ $110,000 = 0.087 or 8.7%.

- Your ROI was 8.7%.

ROI for Financed Transactions

Calculating the ROI on financed transactions is more involved.

For example, assume you bought the same $100,000 rental property as above, but instead of paying cash, you took out a mortgage.

- The downpayment needed for the mortgage was 20% of the purchase price, or $20,000 ($100,000 sales price x 20%).

- Closing costs were higher, which is typical for a mortgage, totaling $2,500 up front.

- You paid $9,000 for remodeling.

- Your total out-of-pocket expenses were $31,500 ($20,000 + $2,500 + $9,000).

There are also ongoing costs with a mortgage:

- Let’s assume you took out a 30-year loan with a fixed 4% interest rate. On the borrowed $80,000, the monthly principal and interest payment would be $381.93.

- We’ll add the same $200 per month to cover water, taxes, and insurance, making your total monthly payment $581.93.

- Rental income of $1,000 per month totals $12,000 for the year.

- Monthly cash flow is $418.07 ($1,000 rent – $581.93 mortgage payment).

One year later:

- You earned $12,000 in total rental income for the year at $1,000 per month.

- Your annual return was $5,016.84 ($418.07 x 12 months).

To calculate the property’s ROI:

- Divide the annual return by your original out-of-pocket expenses (the downpayment of $20,000, closing costs of $2,500, and remodeling for $9,000) to determine ROI.

- ROI = $5,016.84 ÷ $31,500 = 0.159.

- Your ROI is 15.9%.

Home Equity

Some investors add the home’s equity into the equation. Equity is the market value of the property minus the total loan amount outstanding. Keep in mind that home equity is not cash-in-hand. You would need to sell the property to access it.

To calculate the amount of equity in your home, review your mortgage amortization schedule to find out how much of your mortgage payments went toward paying down the principal of the loan. This builds up the equity in your home.

The equity amount can be added to the annual return. In our example, the amortization schedule for the loan showed that a total of $1,408.84 of principal was paid down during the first 12 months.

- The new annual return, including the equity portion, equals $6,425.68 ($5,016.84 annual income + $1,408.84 equity).

- ROI = $6,425.68 ÷ $31,500 = 0.20.

- Your ROI is 20%.

The Importance of ROI for Real Estate

Knowing the ROI for any investment allows you to be a more informed investor. Before you buy, estimate your costs and expenses, as well as your rental income. This gives you a chance to compare it to other, similar properties.

Once you’ve narrowed it down, you can then determine how much you’ll make. If, at any point, you realize that your costs and expenses will exceed your ROI, you may need to decide whether you want to ride it out and hope you’ll make a profit again—or sell so you don’t lose out.

Other Considerations

Of course, there may be additional expenses involved in owning a rental property, such as repairs or maintenance costs, which would need to be included in the calculations, ultimately affecting the ROI.

Also, we assumed that the property was rented out for all 12 months. In many cases, vacancies occur, particularly in between tenants, and you must account for the lack of income for those months in your calculations.

The ROI for a rental property is different because it depends on whether the property is financed via a mortgage or paid for in cash. As a general rule of thumb, the less cash paid up front as a downpayment on the property, the larger the mortgage loan balance will be, but the greater your ROI.

Conversely, the more cash paid upfront and the less you borrow, the lower your ROI, since your initial cost would be higher. In other words, financing allows you to boost your ROI in the short term, as your initial costs are lower.

It’s important to use a consistent approach when measuring the ROI for multiple properties. For example, if you include the home’s equity in evaluating one property, you should include the equity of the other properties when calculating the ROI for your real estate portfolio. This can provide the most accurate view of your investment portfolio.