宾州首富年赚13亿联邦税仅18.7% 低于多数高收入劳工

世界新闻网

4/16/2022

费城询问报(The Philadelphia Inquirer)报导,非营利组织ProPublica发布的数字显示,宾州首富亚斯(Jeff Yass)过去几年平均每年赚13亿元,缴纳的联邦税则是18.7%,低于国内绝大多数高收入劳工。

ProPublica的数字显示,亚斯在2013年至2018年间,平均年收入为13亿元,位居全美第六,次于微软(Microsoft)创办人比尔盖兹(Bill Gates),金融大亨彭博(Michael Bloomberg),WhatsApp创办人库姆(Jan Koum),苹果(Apple)创办人乔布斯(Steve Jobs)遗孀萝林(Laurene Powell Jobs),投资公司Citadel创办人、亚斯的同行竞争对手格里芬(Ken Griffin)。

亚斯在那几年缴纳的联邦税率为18.7%,此数字约与比尔盖兹差不多,比库姆及格里芬还低,但高于彭博及萝林;这可能是因为亚斯只将4%的收入用于合法避税,而彭博及萝林分别把他们66%及51%的收入投到非营利事业中以合法避税。

尽管ProPublica没有计入州及地方税,但此税率依然比绝大多数的高所得劳工还要低,因为在2018年,若夫妻一起申报年收入60万,将被课征37%的联邦所得税;这是因为国内大多数的富豪只会被课征资本利得税,且是在变现的时候才会课征,而美国的资本利得税率基本上又比一般劳工的薪资税率低。

亚斯是投资公司Susquehanna International Group的联合创办人,为自营交易商,投资项目只跟合作伙伴进行,而非向客户提供投资服务。

Susquehanna的投资内容十分多样,从科技股到垃圾债都有,目前最大的投资项目为抖音(TikTok)母公司「字节跳动」;这也成为华尔街的谜团之一,因为Susquehanna在中国是以非营利组织的名义运作,他们是如何在中国严格的监管下将大笔收益带回美国至今依然不明。

亚斯也是宾州著名的政治献金捐助者,而且遍及两党政要,包括前总统川普、联邦参议员保罗(Rand Paul)。

Healthcare Certification and ESL Programs

Billionaires tax faces constitutional, political hurdles

The question for tax writers and party leaders is whether they can thread those needles in drafting the details.

By Jonathan Allen

10/28/2021

WASHINGTON — Democrats’ plan to tax billionaires excites the party’s base. It could be attractive to Sen. Kyrsten Sinema, D-Ariz. And it might be unconstitutional.

Party leaders have been scrambling to find alternative ways to pay for part of the trillion-dollar-plus “Build Back Better” bill because Sinema has ruled out raising income tax rates on high-end earners and corporations.

A proposal released Wednesday morning would tax the paper investment gains of the ultra-wealthy. The idea is to capture revenue from billionaires whose “tradable” assets — like stocks — appreciate in value each year without being taxed. Under current law, those gains aren’t “realized” and taxed until the underlying assets are sold.

The tax would also apply to the tradable assets of people who earn $100 million or more in three consecutive years, but it would not apply to property such as real estate.

An ally of Biden’s, Rep. Brendan Boyle, D-Pa., a member of the tax-writing Ways and Means Committee, has worked on a version of the wealth tax with Sen. Elizabeth Warren, D-Mass. He said in an interview Tuesday that it is easy for the government to tax all of the earned income of workers, while the country’s wealthiest investors can simply earn value by holding on to untaxed investments.

“That ends up being very unfair,” he said, adding that he is confident that the plan would survive constitutional muster.

Tax law experts disagree about whether such a provision would be consistent with the Constitution, but Daniel Hemel, a University of Chicago Law School professor, said Democrats would be taking their chances with a conservative Supreme Court.

“This approach makes the Democrats’ plan for taxing the wealthy contingent upon Brett Kavanaugh, and there are lots of constitutionally uncomplicated ways to tax the very rich,” Hemel said. “But it seems like Democrats are coalescing around one of the approaches for which there are genuine constitutional doubts.”

The question for tax writers and party leaders is whether they can thread both the political and the constitutional needles in drafting the details.

Clear majorities of Americans favor taxing the rich more. In a Morning Consult/Politico poll last month, 68 percent of registered voters said they support raising taxes on the wealthiest people. But few if any independent surveys delve into the question of taxing the unrealized gains of billionaires.

Still, not every Democrat in Congress is sold on the latest approach yet.

“It’s new, so implementation becomes an issue,” said Sen. Jon Tester, D-Mont., who added that he hasn’t passed judgment one way or the other. “I’ve really got to study it.”

Senate Finance Committee Chairman Ron Wyden, D-Ore., the author of the provision, said he is confident that it would survive legal challenges. As proof, he cited lower court rulings in which the taxation of unrealized gains from futures contracts “has always been upheld.”

Legal scholars say that even if courts ruled in favor of taxing unrealized gains at their increased values — known as a “mark to market” assessment of value — it’s unclear how they would approach the constitutionality of a tax conditioned on the wealth of the taxpayer rather than on his or her income.

“There are plausible arguments on both sides,” said Andrew Hayashi, a professor who is the director of the University of Virginia’s Center for Tax Law.

When the Constitution was ratified, it required that “direct taxes” be apportioned among the states “according to their respective numbers,” meaning each state would have to cough up an amount proportional to its population. The 16th Amendment created an exemption that allows the federal government to collect income taxes.

The basic questions for the courts are whether a federal tax can be based in part on wealth and whether paper gains on assets can be taxed as income before they are sold.

From a political perspective, Democratic leaders may end up caring more about whether they can pass the provision than whether it would survive a court challenge. The billionaires tax can’t be ruled unconstitutional unless it has first become law.

However, the possibility that a successful court challenge would add to the deficit could scare off lawmakers who want to ensure that the “Build Back Better” measure remains deficit-neutral. Biden has promoted his plan as having no cost, because its spending would be offset by new revenue, and Sen. Joe Manchin, D-W.Va., a key swing vote on the overall legislation, has emphasized balancing the revenue and spending.

Still, it is easier for Democratic leaders to count votes than it is for them to predict court rulings.

“I’d give it a 50 percent chance,” said Hemel, who called the wealth tax a “good idea” in a Washington Post op-ed. “We’ve got lots of other options that are 100 percent chance.”

富豪税恐违宪 富人宁花数百万打官司 有机会省数10亿

世界新闻网 | 记者颜伶如/综合报导

10/28/2021

民主党快马加鞭推出的富豪加税提议,打算对富豪未变卖持股每年增值课税;华尔街日报分析,这项提议可能面临的最大障碍就是美国宪法,倘若实施,几乎可以确定将面临司法诉讼;富豪纳税人提告的诱因极大,因为花数百万律师费用,有机会省下数十亿税金。

年收入连续3年超过1亿也在内

根据27日上午公布的民主党提议草案,加税对象为全美最有钱富豪的可交易资产(tradable assets),例如每年增值但未脱手卖出的股票;民主党提案适用对象还包括年收入连续三年超过1亿元的民众,房屋等不动产并不在这波加税范围之列。

目前税法规定,资本利得税(capital-gains taxes)是在股票等资产卖出之后才课征;宪法起草时,规定各州依人口比率收取直接税(direct taxes),宪法第16修正案则赋予联邦政府征收个人所得税的权限。

民主党加税提议可能遭逢的反对论点为:对亿万富豪征收未实现资本利得税(unrealized capital gains tax),明显逾越第16修正案范畴。

保守派倡议组织「全国纳税人联盟基音会」 (NTUF)税务政策与诉讼部副总监毕夏普-汉契曼(Joseph Bishop-Henchman)指出,富豪加税没有采循分配税务原则,而且是针对未变卖资产课税,条款还具有强制性,「自然会引发违背宪法的严重质疑。」

加税对象总计不到1000人

符合民主党提议内容的加税对象总计不到1000人,其中包括财产超过10亿元的富豪,以及连续三年个人年收入超过1亿元的民众。

民主党及某些法律学者指出,有信心富豪加税提议符合宪法,可以认定为某种可扣税所得税(allowable income tax)或某种形式的间接税(indirect tax),例如遗产税(estate tax);但如果官司上诉到最高法院,大法官将如何裁定,则是未知数。

华尔街日报指出,宪法虽然赋予国会征税的广泛权限,但对于如何征税却有严格限制,例如规定必须为各州之间分担的直接税(direct taxes);自从南北战争以来,国会都不曾加征过直接税兼分配赋税(apportioned tax )。

最高法院在一项1920年判例当中裁定,某些股息(stock dividends)不能视为收入(income),持股必须出售才算获取资本利得,这项判决迄今并未被完全推翻。

白宫分析:美国最富人纳税额远低于他人

文 / 林煇智

9/23/2021

(早报讯)白宫一份新经济分析报告显示,美国最富人的纳税额远远低于其他人。这份报告将为美国总统拜登推动向富人增税的计划提供有力的支持。

路透社报道,拜登周三(9月22日)在推特上写道:“我对超级富豪和大公司不支付其公平的税收感到厌烦。”

据报道,拜登正在推动一项3.5万亿美元(4.7万亿新元)的法案,该法案将通过让超级富豪和企业缴纳更多税款,扩大联邦在应对气候变化、降低儿童护理成本和减少贫困方面的努力。

白宫两位经济学家的分析表明,全国最富的400个、净资产在21亿美元至1600亿美元之间的家庭,平均每年支付的有效联邦所得税率略高于8%。

报告发现,2010年至2018年,这400个家庭,如果包括其财富价值的上升,总共赚取1.8万亿美元,支付的联邦个人所得税则估计为1490亿美元。

白宫对美国超级富豪和亿万富翁所支付税额的分析远低于其他分析。白宫的税率计算使用了来自国内税收局和美联储消费者财务调查的高收入者的收入、财富和支付的税款数据。

White House: 400 wealthiest families paid average tax rate of 8.2 percent

BY NAOMI JAGODA

9/23/2021

The White House released an analysis on Thursday estimating that the 400 wealthiest American families paid an average federal income tax rate of only 8.2 percent on $1.8 trillion of income from 2010 to 2018.

“Two factors that contribute to this low estimated tax rate include low tax rates on the capital gains and dividends that are taxed, and wealthy families’ ability to permanently avoid paying tax on investment gains that are excluded from taxable income,” the report said.

The analysis, which was authored by economists from the White House Council of Economic Advisers and the Office of Management and Budget, comes as Democrats in Congress are working on a tax-and-spending package that would advance much of President Biden‘s agenda. Biden has proposed a number of tax increases on the wealthy and corporations in order to pay for his spending priorities in areas such as health care and child care, and he is seeking to prevent moderate congressional Democrats from scaling back these proposals.

The White House analysis is based on IRS statistics, the Federal Reserve’s Survey of Consumer Finances, and Forbes magazine estimates about the 400 wealthiest Americans.

The White House noted that its estimate of the tax rate for the wealthiest households is “much lower” than other groups’ estimates of top income tax rates. The administration’s takes into account income from unrealized capital gains, which is not typically included in this type of analysis.

The report highlighted Biden’s proposals to raise the top capital gains rate and end the “stepped-up basis” tax preference that benefits heirs as ways to address the fact that wealthy Americans pay a low tax rate.

Legislation approved by the House Ways and Means Committee earlier this month included a smaller capital gains increase than Biden had proposed and does not repeal stepped-up basis. But Senate Democrats are expected to offer their own ideas for how to pay for the spending package, and Finance Committee Chairman Ron Wyden (D-Ore.) has indicated that he wants to prevent billionaires and their heirs from avoiding taxes on stock gains.

Wyden said in a statement Thursday that “the White House’s new report is shocking but not surprising.”

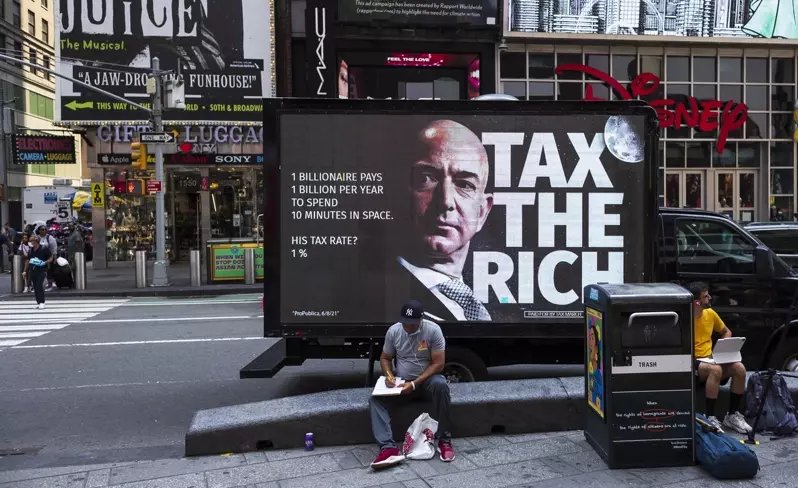

Top 1 Percent Avoid Paying $163 Billion in Taxes Each Year: Treasury Department

By Leia Idliby

9/08/2021

The Department of Treasury has found that the wealthiest one percent of Americans have avoided paying $163 billion in taxes per year.

The Treasury’s analysis, titled “The Case for a Robust Attack on the Tax Gap” and written by Deputy Assistant Secretary for Economic Policy Natasha Sarin, opens by explaining, “A well-functioning tax system requires that everyone pays the taxes they owe.”

The report argues that narrowing the tax gap, which accounts for the difference between owed and collected taxes, will lead to a more equitable economy, as it currently “totals around $600 billion annually,” which would lead to “approximately $7 trillion of lost tax revenue over the next decade.”

Sarin’s report includes a table detailing tax data from 2019, which ultimately found that more than $160 billion lost annually is “from taxes that top 1 percent choose not to pay.”

The report goes on to argue that in order to collect owed taxes and enforce laws against high earners and corporations, the IRS needs funding to update their technology and to hire agents able to decipher “thousands of pages of sophisticated tax filings.”

“It also needs access to information about opaque income streams — like proprietorship and partnership income — that accrue disproportionately to high-earners,” she wrote.

The reports comes as President Joe Biden’s administration is pushing for a significant increase to the IRS budget. The White House has specifically called for $80 billion of investment over the next ten years, claiming it would help the government catch tax evasion schemes.

“Giving the IRS the information and resources that it needs will generate substantial revenue,” Sarin concluded. “But even more importantly, these reforms will create a more equitable, efficient tax system.”

Top 0.1% Tap Private Placement Life Insurance to Avoid Biden’s Taxes

Financial Advisor IQ

9/04/2021

The richest Americans who want to avoid paying higher taxes under President Joe Biden are tapping a niche product that has become more generally available, cheaper and flexible in recent months.

Some advisors who cater to the top 0.1% say that private placement life insurance is “dominating conversations,” according to Bloomberg.

Assets held in PPLI policies are tax-free, and when a policyholder dies, their heirs inherit the policy’s contents tax-free, Bloomberg writes. Assets inside a PPLI can also be brorrowed against or rolled into another insurance product, according to the news service.

PPLI policies, however, have complicated rules to qualify as life insurance to take advantage of the tax benefit, can fail if not properly funded and taking assets out comes with a heavy tax burden, Bloomberg writes.

“Clients are very interested in this right now,” said Tara Thompson Popernik, director of research for Bernstein Private Wealth Management’s wealth planning and analysis group, according to Bloomberg. “It takes some education to get them to wrap their heads around the concept, because it’s not just buying life insurance.”

But it’s not just the threat of Biden going after billionaires and millionaires to pay their “fair share” that’s making the loophole: a late-2020 insurance law change made PPLI “more powerful,” while competition among insurers has pushed down costs while increasing the choice of products, according to Bloomberg.

“Private placement life insurance poses a serious obstacle to President Biden’s goal of guaranteeing that high-income individuals pay tax on large gains at least once per lifetime,” said Daniel Hemel, a law professor at University of Chicago, according to the news service. “PPLI is a massive loophole — entirely legal, easy to exploit, and politically very hard to close.”

How Does Private Placement Life Insurance Work?

By Maxime Croll

9/04/2021

Private placement life insurance (PPLI) is a niche solution designed for wealthy individuals in high tax brackets who have a few million dollars available to commit.

Many times, those for whom PPLI was designed want to invest in hedge funds, but hedge funds can carry significant taxes: If the wealthy individual invests in them in their personal name, in a taxable account or in a trust, every trade the manager makes can generate a capital gains distribution, and any ordinary income is taxable at particularly high rates.

That’s a serious issue at higher income levels, where combined federal and state income and capital gains taxes can easily add up to nearly 50% in some jurisdictions.

One increasingly popular solution: Hold these assets within a life insurance policy.

Who does private placement life insurance make sense for?

PPLI isn’t for everybody. A good candidate for this strategy is someone with annual income in the millions, a net worth of $20 million or more or someone who controls a business that puts them in that category.

Life insurance comes with a number of important tax benefits, which can be major considerations for those in the highest tax brackets. But standard life insurance policies you can get from your neighborhood agent don’t contain the hedge funds, funds of funds and other alternative investments that these investors require for their own diversification and investment needs.

That’s where privately placed life insurance comes in: Wealthy families, family foundations, trusts, corporations and banks work with hedge funds and money management firms to create their own life insurance contracts, designed to reduce their tax burdens.

The idea is to combine the financial advantages of highly taxed hedge funds and similar investments with the tax advantages of life insurance. There are insurance and administrative costs associated with the life insurance contract, but the tax savings in a properly structured life insurance policy, plus the death benefit itself, more than make up for the additional insurance and administrative costs. And the insured can generally access most of the funds anyway, tax-free, via policy withdrawals and loans.

When a wealthy investor in a very high tax bracket wants to invest in hedge funds anyway, it often makes sense to create a privately placed life insurance policy to shelter the individual from taxes.

Qualifications to purchase PPLI

While anyone can buy a variable universal life insurance policy (as PPLIs are structured), PPLIs are an unregistered securities product. As such, agents can only present them to accredited investors.

Under current Securities and Exchange Commission (SEC) regulations, accredited investors are those with a net worth of at least $1 million (excluding primary residence), or income of at least $200,000 in each of the preceding two years. Married couples must demonstrate income of $300,000 in each of the preceding two years.

Ultimately, the owner is typically an individual or a trust. Holding the policy in an irrevocable trust allows the insured to keep the policy out of their taxable estate, possibly reducing eventual estate tax liability, though they give up rights to access the cash value prior to death.

In reality, the typical PPLI candidate or family has:

- A high net worth

- The ability to fund $1 million or more in annual premiums for several years, at least — $3 million to $5 million is typical

- A desire for hedge fund or alternative investment exposure

- Highly tax-inefficient investments

- High state and local income taxes in addition to federal (advisors should be alert to the effect of any state premium taxes on the strategy)

- A desire to shelter assets from creditors

It’s important to be able to make a significant investment over the first several years as this initial investment of premium “primes the pump,” meaning that, assuming the underlying investment subaccounts perform adequately, the insured’s policy can become self-funding. That is, growth in its cash value covers the cost of insurance. At that point, the insured can cease committing premium if they choose.

Where to buy private placement life insurance

Professional wealth managers tend to recommend vendors. However, some of the most prominent providers of PPLI services and insurance-dedicated funds (IDFs) include BlackRock, Wells Fargo Private Banking, John Hancock, Zurich, Crown Global and Pacific Life.

How private placement life insurance works

Privately placed life insurance is generally structured as a variable universal life insurance policy, meaning:

- Premiums are flexible. Policyholders can pay as much or as little premium as they like, whenever they like.

- The cost of insurance is deducted from the cash value in the policy subaccounts each month or each year.

- To keep the policy in force, the owner must pay enough premium to maintain enough cash value to cover the cost of insurance.

- If the cash value reaches zero, the policy will lapse.

The agent who sets it up will usually structure the policy to maximize cash value accumulation while keeping the death benefit (and thus the cost of insurance) relatively low. The policy owner, working with their insurance professional, then pays as much premium into the policy as possible every year.

The client gets the benefit of the tremendous tax advantages of the life insurance contract:

- Tax-free death benefits to heirs

- Tax-deferred growth of cash value

- Tax-free growth of dividends (if applicable)

Meanwhile, the insured still has access to accumulated cash values, which can be used for any purpose and accessed at any age. There are no penalties for accessing the cash value before turning age 59 1/2, as there are with annuities and with individual retirement accounts (IRAs). In addition, there are no required minimum distributions, as there are with annuities, IRAs and retirement accounts.

PPLI investments

As discussed, the best investment candidates for a PPLI policy are those that are tax-inefficient. They generate substantial current taxable income, imputed (phantom) income or capital gains unless they are held in a retirement account or life insurance vehicle that provides tax-free growth.

PPLI owners and their advisors either choose specific investments for their portfolios or carefully select money managers to manage their portfolios within the policies. Possible investments can include venture capital, real estate investment trusts, private equity funds, funds of hedge funds and commodity funds, or any fund with extremely high turnover rates that generate substantial short-term capital gains.

But that doesn’t mean anything goes. PPLIs must still meet IRS standards for investor control, insurance and diversification.

Investor control. Individual policy owners and family offices are prohibited from exercising influence over the specific investment decisions of the fund managers. If the owner exercises too much control, the IRS may disqualify the tax advantages of the policy. Current case law requires managers to operate on an independent, discretionary basis. Assets held in PPLI policies are not designed to be separately managed accounts, and they should not be treated that way.

Insurance standards. The life insurance structure allows owners to sell insurance-dedicated funds within the policy as often as they like and replace them with other qualified investments, without tax consequences. IDFs are financial products that are designed specifically for the PPLI market. Hedge funds and funds of funds often create a version of their flagship offering as an IDF that uses all the same strategies and managers but is also managed to adhere to laws and regulations that govern insurance portfolios.

Diversification requirements. Investments must also meet diversification rules:

- No single investment may make up more than 55% of the insurance subaccount portfolio.

- No two investments may constitute more than 70% of the portfolio.

- No three investments may constitute more than 80% of the portfolio.

- No four investments may constitute more than 90% of the total assets of the account.

Therefore, the portfolio must, in practice, contain a minimum of five distinct investments in order to fully qualify as life insurance. Otherwise, the IRS will disqualify the policy, and the owner will lose the tax advantages of the life insurance structure.

Accessing your money in a PPLI

Policy owners can withdraw from their cash value or borrow against it at any time, for any purpose.

Withdrawals Withdrawals are tax-free up to the basis of the policies. So owners can get back their premiums, minus fees, without tax consequences — as long as their subaccounts’ performance has kept up with the cost of insurance. If the cash value is greater than the owner’s basis in the policy — that is, what they have paid in — then additional withdrawals in excess of basis are taxed as a gain.

Policy loans You can borrow against the cash value of the policy with no underwriting or credit check. The loan is secured by the policy’s cash value. This makes the policy a solid choice for emergency funds. The loan does not have to be paid back, though the policy owner may want to replenish funds borrowed from the policy so as to maximize long-term tax-free growth.

Because the loans are secured by payments already made to the insurer, interest rates are often very low. Borrowers should be aware that interest does accrue, and borrowing will reduce any death benefits paid out unless the loan is paid back to the policy.

Contribution limitations and modified endowment contracts

The government imposes limits to how much premium the owner can contribute to the policy in a given year in order to help ensure life insurance is used for its intended purpose, as opposed to a tax shelter. The result of the contribution limit is the “seven-pay” test. If policyholders contribute so much premium to their policies that the policy would be paid up in less than seven years, it becomes a modified endowment contract (MEC). This will disqualify the policy from many of the tax advantages on withdrawals and loans:

- One of the great things about insurance policies is that when you withdraw cash value from an in-force life insurance policy, you get the benefit of first-in, first-out (FIFO) taxation. This allows you to withdraw as much as you’d like, up to your basis in the policy (the amount you have contributed), tax-free. If your policy becomes an MEC, this advantage disappears. Instead, the IRS will deem you to be withdrawing interest first, not your basis. This interest is taxable.

- Likewise, while the law allows you to take tax-free loans from a life insurance policy, once your policy becomes an MEC, those loans become taxable as income.

- Additionally, once your policy becomes an MEC, any withdrawals prior to age 59 1/2 become subject to a 10% early withdrawal penalty, just as with a qualified annuity or a 401(k).

Your policy documents should specify the annual MEC limit.

| Life insurance contract | MEC | |

|---|---|---|

| Premiums | Limited by seven-pay test | Not limited except by contract |

| Loans | Tax-free for life of policy | Taxable as income |

| Withdrawals | Tax-free up to basis (FIFO) | Taxable until all interest/gains are withdrawn |

| Death benefit | Tax-free | Tax-free |

| Death benefit amount | Usually kept small in PPLI to maximize growth of cash value | Used to maximize death benefit |

How are PPLI policies different from retail life insurance?

Structurally, privately placed life insurance is identical to a conventional variable universal life insurance policy. What sets the PPLI apart is the assets held in the subaccount: An everyday retail customer will choose from a limited menu of subaccount investments offered by the life insurance company.

But when you buy a PPLI, you can customize your investment subaccounts. You can include nearly any investment imaginable — from index funds to hedge funds. Your registered investment advisor or wealth manager can help design the investments in your menu of subaccounts.

Tax and other benefits of PPLI

High-income individuals are very tax-sensitive. The ordinary income tax rate on incomes above $518,401 in 2018 was 37%, plus additional Affordable Care Act taxes on high-income individuals. When you add in state and local income taxes in some jurisdictions, the income tax bite for high-income families could add up to nearly 50%.

The heart of the PPLI strategy lies in the tax advantage. The PPLI essentially converts a very tax-inefficient investment, such as a hedge fund, into a very tax-efficient one for the high-net-worth investor.

| Hedge fund held in personal account (typically) | Hedge fund held within a PPLI | |

|---|---|---|

| Death benefit | N/A | Tax-free death benefit |

| Income | Taxable at 37%-50% | Tax-free for life of policy |

| Short-term capital gains | Taxable at 37%-50% | Tax-free for life of policy |

| Long-term capital gains | Taxable at 20% | Tax-free for life of policy |

| Imputed income | Taxable at 37%-50% | Tax-free for life of policy |

| Transfers to other life policies | Taxable, gain over basis | Tax-free under IRC Section 1035 |

| Transfer to annuities | Taxable, gain over basis | Tax-free under IRC Section 1035 |

| Creditor protection | None | Enhanced |

| Estate tax treatment | Taxable unless in irrevocable trust | Taxable in estate of owner unless in irrevocable life insurance trust |

| Tax loss harvesting strategies | Investors can sell losers to offset capital gains | N/A, though losing policies can be surrendered |

| Treatment at death | Subject to probate | Bypasses probate — death benefit goes to beneficiaries in a matter of days |

This strategy neutralizes the impact of current income by placing the assets within a life insurance policy, with tax advantages similar to a Roth IRA. Assets within the policy enjoy tax-free growth for as long as they remain in the policy.

In addition to the tax benefits that generally accrue to life insurance cash values, PPLI policies often provide a number of additional benefits:

- Lower commissions. The cost of insurance and commissions is low compared to most retail life insurance products: Issuers are more interested in managing your money than in generating large upfront commissions.

- No surrender charges. Because they don’t rely on a commission-paid insurance sales force as traditional insurance companies do, they don’t need to recoup commission costs by imposing surrender charges.

- Phantom income is not taxed. Some investments generate a tax liability to the owner, even though there is no actual cash income distributed. For example, a zero-coupon bond pays no income until it matures, but the IRS forces taxpayers to pay taxes on imputed income as the bond approaches maturity. If the asset is held in a PPLI, the tax on imputed or phantom income is neutralized.

- Tax compliance is easier. Tax reporting is a constant headache for hedge fund investors and those who hold interests in limited partnerships and master limited partnerships. By holding these assets within a PPLI, the taxpayer can eliminate having to deal with K-1 reports and other reporting requirements.

- Creditor protection. Cash value life insurance is a proven way to shelter assets from creditors. Life insurance and annuities enjoy substantial asset protection in every state, and in some states, like Florida and Texas, creditor protection is unlimited. In some cases, PPLI life insurance assets are held offshore — placing these assets out of the reach of U.S. courts. No U.S. court can force a foreign company to release funds to a creditor.

新媒体广告策划

往微信群丢名片、砸海报、甩二维码

瞬间被踢飞,或者没人理?

资讯软文营销

你的文案专家

无论你是房地产经销、贷款专员,

还是保险经纪,或从事其他行业

我们将为你——

根据投放渠道、匹配群主题

打包定制资讯类带广告文案

配套地区、行业渠道投放

千群代发,精准推广

为你的事业助推

可扫码加小编微信:↓