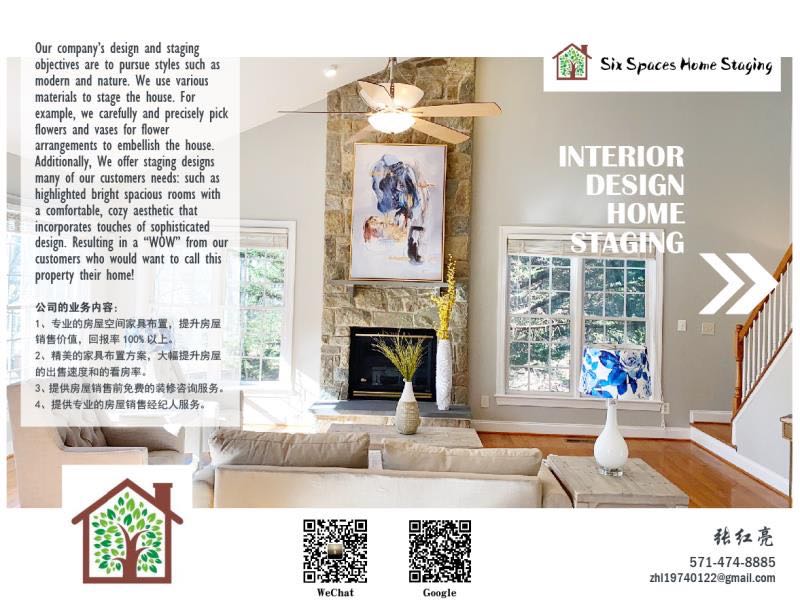

Six Spaces Home Staging

Contact: Hongliang Zhang

Tel: 571-474-8885

Email: zhl19740122@gmail.com

The Housing Market Continues To Cool. What Will This Fall Be Like?

By Clare Trapasso

8/26/2021

The forecast for the coming months is lower temperatures—and a cooler real estate market, if only by a few degrees.

The housing market is expected to shift to something closer to normal this fall, real estate experts say. They anticipate more homes will go up for sale, helping to slow down the unparalleled price increases and bidding wars of the past year.

But the market is likely to remain highly competitive, as there will still be many more buyers than homes to go around.

“We’re going to exhaust the pool of buyers who are still sitting on a lot of cash looking to buy their next home,” says Realtor.com® Senior Economist George Ratiu. “The market does not have a magical way of sustaining this pace [of price growth], because you’re going to run out of people who can afford it.”

Tel: 551-580-4856 | Email: F.WINNIE.S@GMAIL.COM

However, that doesn’t mean that home prices, whose national median hit an all-time high of $385,000 in the week ending Aug. 14, will fall. In fact, prices increased 8.6% year over year that week. But that’s significantly less than the 17.2% annual rise in April. Going into the end of the year, prices may rise a more modest 5% to 6%, says Ratiu.

“The shift in the housing market will make shopping for a home a lot more tolerable than it has been, because consumers will actually have time to properly think through their decision and won’t be in as fierce of bidding wars,” says Ali Wolf, chief economist of building consultancy Zonda. “Going into fall, buyers may not need to pull out all the stops to win a house, like removing the inspection contingency or waiving the appraisal contingency.”

More homes are expected to go up for sale in the second half of the year. The influx won’t be nearly enough to put a dent in the dire housing shortage that’s the main reason for the record prices, but it may help curb the wild price growth.

“It’s still going to be a very strong housing market. Demand is still going to be well in excess of supply,” says Greg McBride, chief financial analyst at Bankrate.com. “It just won’t be as frenetic as what had been experienced earlier in the year.”

In June, there were 2.6 months of housing inventory for sale, according to the National Association of Realtors®. That’s an improvement from 1.9 months in January. However, a balanced real estate market has between 5.5 months and six months of homes for sale.

“We’re seeing the gap narrowing between demand and supply,” says NAR’s director of housing and commercial research, Gay Cororaton. But it isn’t going to even out anytime soon. “There’s still a huge, huge gap.”

The fall homebuying season is likely to be busier than usual

One thing that won’t return to usual is the pace of sales. Usually, the market begins slowing down and prices even dip in the fall; families typically prefer to get settled before the school year begins. But this year, the COVID-19 pandemic threw off the normal timing, and activity is expected to stay brisk after summer’s end.

“I expect an unusually busy fall season,” says Ratiu. After all, more homeowners are vaccinated and feel comfortable holding open houses, although the delta variant of the coronavirus could change this, or they just can’t delay their move. “Sellers are putting homes on the market. Normally this activity happens early in the spring.”

Demand is likely to stay strong as well—even though many buyers are frustrated or simply priced out. More millennials are hitting their prime homebuying years, and builders have been unable to ramp up construction to keep up with the growing population. With rental prices also hitting new heights, many people are seeing that it’s cheaper to buy than to continue to lease a home.

Plus, mortgage interest rates are still hovering around record lows. The fear of missing out on what could be a once-in-a-lifetime deal will likely entice additional buyers. (Rates averaged 2.87% for 30-year fixed-rate mortgages in the week ending Aug. 12, according to Freddie Mac data.)

And not every home will be affected by a slowdown.

“Don’t expect deals in the fall if you are house hunting in the most desirable part of a market or competing for a particularly nice house,” says Zonda’s Wolf. “Homes that stand out for one reason or another are still flying off the shelf.”

But overall, most buyers may not be as willing to pay top dollar and waive inspections and contingencies for less-than-spectacular homes that would have sold for $100,000 less just a year ago. There aren’t many regular people (as opposed to investors) who can pay all cash for a home. And there likely aren’t as many remote workers fleeing expensive cities and heading for cheaper parts of the country at this point in the pandemic as there were in the beginning.

“We are definitely shifting from an extreme excess of demand to a more moderate excess of demand,” says Ken Rosen, chair of the Fisher Center for Real Estate and Urban Economics at the University of California, Berkeley. But “it’s still going to be a seller’s market.”

In addition, many first-time buyers can’t afford to pay over the list price of a home if it doesn’t appraise for that much, says mortgage broker Rocke Andrews, of Lending Arizona in Tucson. They don’t have the extra cash to make up the difference.

The emergence of the delta variant is also spooking some buyers who worry about the stability of their jobs.

This could help to explain why the number of purchase mortgages (which don’t include refinances) dropped 18.7% year over year in the week ending Aug. 13, according to the most recent Mortgage Bankers Association data.

The market “will be nothing like the panic we saw” going into the fall, says Rosen. “It already is more orderly in many, many markets.”

Foreclosures likely won’t play a big part in the cooling market

Many folks have been anticipating a wave of foreclosures to sweep the country as moratoriums to protect struggling homeowners expire. However, it’s not expected to be nearly as severe as what happened during the Great Recession, or lead to an influx of homes going on the market.

Homeowners who haven’t made mortgage payments during the pandemic make up just a fraction of the housing stock—just 3.26% of mortgages were in forbearance as of Aug. 8, according to the most recent data from the Mortgage Bankers Association. Many of these folks will resume payments or work something out with their lenders. But at least some of these 1.6 million homes will hit the market.

Those homeowners who can’t resume their monthly payments and have enough equity in their properties can avoid foreclosure by putting their homes on the market. With prices at these levels, they may even walk away with a profit, and it won’t damage their credit.

“The middle-class and the upper-income groups won’t even notice the wave of foreclosures because it won’t be in their neighborhoods,” says Norm Miller, a real estate economics professor at the University of San Diego.

Lower-income homeowners who lost their jobs during the pandemic and don’t have much equity will likely be the ones who go into foreclosure. Their homes are expected to be in the lower-third price tier.

The number of foreclosures and how quickly they go up for sale are expected to vary from state to state. Some states have protections in place for homeowners that can delay proceedings significantly.

Some first-time buyers will scoop up these properties as the previous owners are forced back into the rental market. But the bulk are expected to go to investors, says Miller.

Investors are expected to keep home prices strong. During the pandemic, more institutional investors, such as pension funds and financial firms, have bought up single-family homes to turn them into rentals. Many can buy in bulk and pay in cash. That’s likely to continue.

“This is going to lower the homeownership rate a little as [these residences] become rental units,” says Miller.

Four-day week ‘an overwhelming success’ in Iceland

BBC

7/06/2021

Reykjavík City Council took part in the trial

Trials of a four-day week in Iceland were an “overwhelming success” and led to many workers moving to shorter hours, researchers have said.

The trials, in which workers were paid the same amount for shorter hours, took place between 2015 and 2019.

Productivity remained the same or improved in the majority of workplaces, researchers said.

A number of other trials are now being run across the world, including in Spain and by Unilever in New Zealand.

In Iceland, the trials run by Reykjavík City Council and the national government eventually included more than 2,500 workers, which amounts to about 1% of Iceland’s working population.

A range of workplaces took part, including preschools, offices, social service providers, and hospitals.

Many of them moved from a 40 hour week to a 35 or 36 hour week, researchers from UK think tank Autonomy and the Association for Sustainable Democracy (Alda) in Iceland said.

The trials led unions to renegotiate working patterns, and now 86% of Iceland’s workforce have either moved to shorter hours for the same pay, or will gain the right to, the researchers said.

Workers reported feeling less stressed and at risk of burnout, and said their health and work-life balance had improved. They also reported having more time to spend with their families, do hobbies and complete household chores.

Will Stronge, director of research at Autonomy, said: “This study shows that the world’s largest ever trial of a shorter working week in the public sector was by all measures an overwhelming success.

“It shows that the public sector is ripe for being a pioneer of shorter working weeks – and lessons can be learned for other governments.”

Gudmundur Haraldsson, a researcher at Alda, said: “The Icelandic shorter working week journey tells us that not only is it possible to work less in modern times, but that progressive change is possible too.”

Spain is piloting a four day working week for companies in part due to the challenges of coronavirus.

And consumer goods giant Unilever is giving staff in New Zealand a chance to cut their hours by 20% without hurting their pay in a trial.

In May, a report commissioned by the 4 Day Week campaign from Platform London suggested that shorter hours could cut the UK’s carbon footprint.

Source: https://www.bbc.com/news/business-57724779

Federal Communications Commission

Emergency Broadband Benefit

The Emergency Broadband Benefit is an FCC program to help families and households struggling to afford internet service during the COVID-19 pandemic. This new benefit will connect eligible households to jobs, critical healthcare services, virtual classrooms, and so much more.

About the Emergency Broadband Benefit

The Emergency Broadband Benefit will provide a discount of up to $50 per month towards broadband service for eligible households and up to $75 per month for households on qualifying Tribal lands. Eligible households can also receive a one-time discount of up to $100 to purchase a laptop, desktop computer, or tablet from participating providers if they contribute more than $10 and less than $50 toward the purchase price.

The Emergency Broadband Benefit is limited to one monthly service discount and one device discount per household.

Who Is Eligible for the Emergency Broadband Benefit Program?

A household is eligible if a member of the household meets one of the criteria below:

- Has an income that is at or below 135% of the Federal Poverty Guidelines or participates in certain assistance programs, such as SNAP, Medicaid, or Lifeline;

- Approved to receive benefits under the free and reduced-price school lunch program or the school breakfast program, including through the USDA Community Eligibility Provision in the 2019-2020 or 2020-2021 school year;

- Received a Federal Pell Grant during the current award year;

- Experienced a substantial loss of income due to job loss or furlough since February 29, 2020 and the household had a total income in 2020 at or below $99,000 for single filers and $198,000 for joint filers; or

- Meets the eligibility criteria for a participating provider’s existing low-income or COVID-19 program.

How to Apply

The online application for the Emergency Broadband Benefit Program is experiencing high demand. We appreciate your patience as we actively work to resolve any connectivity issues users may encounter.

Apply Now

There are three ways for eligible households to apply:

- Contact your preferred participating broadband provider directly to learn about their application process.

- Go to GetEmergencyBroadband.org to apply online and to find participating providers near you.

- Call 833-511-0311 for a mail-in application, and return it along with copies of documents showing proof of eligibility to:

Emergency Broadband Support Center

P.O. Box 7081

London, KY 40742

After receiving an eligibility determination, households can contact their preferred service provider to select an Emergency Broadband Benefit eligible service plan.

Get More Consumer Information

Check out the Broadband Benefit Consumer FAQ for more information about the benefit.

Which Broadband Providers Are Participating in the Emergency Broadband Benefit?

Various broadband providers, including those offering landline and wireless broadband, are participating in the Emergency Broadband Benefit. Find broadband service providers offering the Emergency Broadband Benefit in your state or territory.

Broadband providers can find more information about how to participate here.

Source: https://www.fcc.gov/broadbandbenefit

Evictions During COVID-19: Landlords’ Rights and Options When Tenants Can’t Pay Rent

Tips, resources, and advice for landlords whose tenants aren’t able to pay the rent due to the coronavirus outbreak.

By Ann O’Connell, Attorney

11/01/2020

Many renters are facing financial challenges resulting from coronavirus-related business shut-downs, furloughs, layoffs, and stay-at-home orders. The longer this crisis goes on, the more likely it is that many will not be able to pay their rent. When renters default on rent, landlords suffer, and might not be able to meet their own financial obligations, such as making the mortgage payments on the rental property.

Here are some suggestions about how landlords can mitigate the financial impact of tenant defaults during the COVID-19 outbreak.

Terminations and Evictions

Under normal circumstances, when tenants don’t pay rent, landlords have the option of terminating the tenancy (by serving the tenant with either a pay rent or quit notice or an unconditional quit notice, depending on the applicable laws). When tenants don’t pay the rent or move out by the deadline given in the notice, landlords can then file an eviction lawsuit to have the tenants physically removed from the rental.

However, health and safety concerns due to COVID-19 have led many states, cities, counties, and courts to place moratoriums on evictions. The scope of these temporary bans on evictions varies greatly: some have banned any and all action relating to evictions, while others simply postpone hearings on evictions until the court can arrange a hearing via telephone or video.

If you are a landlord in an area with an eviction moratorium, you might still be able to file eviction papers with the court, but your case might not be heard for a while. However, even if there are no bans in place, evicting tenants who can’t pay the rent due to the coronavirus crisis probably shouldn’t be your first recourse. Aside from optics (you don’t want to get a reputation as the ruthless landlord who booted tenants out of their home in the middle of a stay-at-home order), if you remove tenants right now, you’re going to be faced with having to disinfect the rental, advertise the rental, screen new prospective tenants (of which there might be very few), sign a new lease or rental agreement, and get the new tenants moved in—all while taking measures to abide by emergency guidelines and health and safety measures.

Consider the following options instead.

Evaluate Your Personal Financial Situation

Take a moment to evaluate your own finances. As dire as it sounds, it might be time to take stock of what could happen in a worst-case scenario. Most landlords have likely considered the situation where tenants don’t pay rent, as this can happen at any time. But there’s no denying that this is a different situation—what will happen if your tenants can’t pay for a long time, and your options for finding new (paying) tenants are slim?

Your assessment of how this worst-case scenario will affect your ability to pay your mortgage (if any) and your personal bills will inform how you respond when your tenants can’t pay their rent.

- If your financial situation looks grim: If your ability to pay the mortgage on your rental property hinges on month-to-month rental income, you should take actions to prevent your own default This includes options discussed below, such as contacting your lender and proactively seeking arrangements with tenants that allow them to make at least partial payments.

- If you have a few months’ reserves: If your personal reserves or financial position won’t feel too much of a pinch if tenants aren’t able to pay rent for a while, you still might have to make some compromises to retain good tenants. If you have tenants who have previously been reliable and are simply finding it hard to make ends meet currently, do what you can to take some pressure off them—see the discussion below about working out a temporary solution with tenants.

Try to Work Out a Temporary Solution With Tenants

Depending on how desperately you need to receive income from your rental, you have a few options for working with tenants who aren’t able to pay rent because of COVID-19. Consider the following possible arrangements.

- Forgive rent. If your situation allows for it, you could waive rent for a month, with an agreement to revisit the payment arrangement on a certain date. A landlord in Bakersfield recently did this for his tenants.

- Postpone rent. You could offer to postpone rent payments for a month, with an agreement that it will be repaid. Your repayment arrangement could state that the rent owed could be spread out over time, paid all at once, or paid when (if) a stimulus check

- Reduce rent. If you can, consider dropping the rent temporarily to a level that enables you to meet your obligations but forgoes profit for the time being. For example, if you normally collect $1200 a month, but your mortgage is $900 a month, you could temporarily drop rent to $900 to make sure you at least don’t get in trouble with your lender.

Before deciding to make any of these adjustments, try talking to your tenants. Ask them straight out what they think they can make work. If you’re able to accommodate their suggestions, chances are higher that they will do everything they can to hold up their end of the bargain. Be sure to put any agreements in writing, preferably as an addendum to your current lease or rental agreement that includes all details of the arrangement.

Look for Outside Assistance

Even if you think you can float a month or two without rental income, you still might want to consider taking some measures now to protect your position in the event that the coronavirus crisis lasts longer than your cushion can handle. If you’re already feeling the pinch, take these actions immediately.

Attend to Your Mortgage

At this point in the COVID-19 crisis, most private lenders are willing to work with borrowers to ensure that they don’t lose their homes. Call your lender directly and ask what steps it is taking to assist borrowers who can’t meet their mortgage obligations due to the coronavirus pandemic.

- If your loan is owned by Fannie Mae or Freddie Mac, you might be able to delay making payments for a certain period of time without incurring late fees or getting hit with a credit score penalty.

- Look into your options under the Coronavirus Aid, Relief, and Economic Security Act.

- The Federal Housing Administration (FHA) has put in place a foreclosure moratorium for single family homeowners with FHA-insured mortgages.

- Visit your state’s website to find out if the state is offering assistance to homeowners. For example, New York has announced a delay of mortgage payments for 90 days. Many other states are postponing any foreclosure actions indefinitely. Find your state’s website at State and Government on the Net.

Look Into Property Tax Breaks

Some states and counties are extending the deadline for paying property taxes, or cancelling late fees and interest. Check your county’s tax assessor’s website to see if this is an option where your property is located.

Seek a Loan

Consider seeking a loan from family, friends, or private lenders. The U.S. Small Business Administration might be another source of assistance—its disaster loan assistance web page has a wealth of information. You can also contact your regular bank or credit union and inquire about what assistance it can offer.

Research Options for Your Renters

Some areas are beginning to offer rent vouchers or emergency funds to renters in need. For example, the Pennsylvania Apartment Association is collecting donations for funds to give to renters who can’t pay rent. Currently, renters’ needs are getting a lot more attention in the press than landlords’ needs, and there are already a lot more resources being made available for renters. It’s in your best interest to research these options and bring them to your renters’ attention—do what you can to help your tenants pay you.

Landlords are getting squeezed between tenants and lenders

By ANNE D’INNOCENZIO

NEW YORK (AP) — When it comes to sympathetic figures, landlords aren’t exactly at the top of the list. But they, too, have fallen on hard times, demonstrating how the coronavirus outbreak spares almost no one.

Take Shad Elia, who owns 24 single-family apartment units in the Boston area. He says government stimulus benefits allowed his hard-hit tenants to continue to pay the rent. But now that the aid has expired, with Congress unlikely to pass a new package before Election Day, they are falling behind.

Heading into a New England winter, Elia is worried about such expenses as heat and snowplowing in addition to the regular year-round costs, like fixing appliances and leaky faucets.

Elia wonders how much longer his lenders will cut him slack.

“We still have a mortgage. We still have expenses on these properties,” he said. “But there comes a point where we will exhaust whatever reserves we have. At some point, we will fall behind on our payments. They can’t expect landlords to provide subsidized housing.”

The stakes are particularly high for small landlords, whether they own commercial properties, such as storefronts, or residential properties such as apartments. Many are borrowing money from relatives or dipping into their personal savings to meet their mortgage payments.

The big residential and commercial landlords have more options. For instance, the nation’s biggest mall owner, Simon Property Group, is in talks to buy J.C. Penney, a move that would prevent the department store chain from going under and causing Simon to lose one of its biggest tenants. At the same time, Simon is suing the Gap for $107 million in back rent.

Michael Hamilton, a Los Angeles-based real estate partner at the law firm O’Melveny & Myers, said he expects to see more retail and other commercial landlords going to court to collect back rent as they get squeezed between lenders and tenants.

Residential landlords are also fighting back against a Trump administration eviction moratorium that protects certain tenants through the end of 2020. At least 26 lawsuits have been filed by property owners around the country in places such as Tennessee, Georgia and Ohio, many of them claiming the moratorium unfairly strains landlords’ finances and violates their rights.

Apartment dwellers and other residential tenants in the U.S. owe roughly $25 billion in back rent, and that will reach nearly $70 billion by year’s end, according to an estimate in August by Moody’s Analytics.

An estimated 30 million to 40 million people in the U.S. could be at risk of eviction in the next several months, according to an August report by the Aspen Institute, a nonprofit organization.

Jessica Elizabeth Michelle, 37, a single mother with a 7-month-old baby, represents a growing number of renters who are afraid of being homeless once the moratorium on evictions ends.

The San Francisco resident saw her income of $6,000 a month as an event planner evaporate when COVID-19 hit. Supplemental aid from the federal government and the city helped her pay her monthly rent of $2,400 through September. But all that has dried up, except for the unemployment checks that total less than $2,000 a month.

For her October rent, she handed $1,000 to her landlord. She said her landlord has been supportive but has made it clear he has bills to pay, too.

“I never had an issue of paying rent up until now. I cry all night long. It’s terrifying,” Michelle said. “I don’t know what to do. My career was ripped out from under me. It’s gotten to the point of where it’s like, ‘Am I going to be homeless?’ I have no idea.’”

Some landlords are trying to work with their commercial or residential tenants, giving them a break on the rent or more flexible lease terms. But the crisis is costing them.

Analytics firm Trepp, which tracks a type of real estate loan taken out by owners of commercial properties such as offices, apartments, hotels and shopping centers, found that hotels have a nearly 23% rate of delinquency, or 30 days overdue, on their loans, while the retail industry has a 14.9% delinquency rate as of August.

The apartment rental market has so far navigated the crisis well, with a delinquency rate of 3%, according to Trepp. That’s in part because of the eviction moratorium, along with extra unemployment benefits from Washington that have since expired.

“There are bad actors, but the majority of landlords are struggling and are trying to work with a bad situation,” said Andreanecia M. Morris, executive director of HousingNOLA, a public-private partnership that pushes for more affordable housing in the New Orleans area.

Morris, who works with both landlords and tenants, said that government money wasn’t adequate to help tenants pay their rent, particularly in expensive cities. She is calling for comprehensive rental assistance.

She fears that residential landlords will see their properties foreclosed on next year, and the holdings will be bought by big corporations, which are not as invested in the neighborhoods.

Gary Zaremba, who owns and and manages 350 apartment units spread out over 100 buildings in Dayton, Ohio, said he has been working with struggling tenants — many of them hourly workers in restaurants and stores — and directs them to social service agencies for additional help.

But he is nervous about what’s next, especially with winter approaching and the prospect of restaurants shutting down and putting his tenants out of work. He has a small mortgage on the buildings he owns but still has to pay property taxes and fix things like broken windows or leaky plumbing.

“As a landlord, I have to navigate a global pandemic on my own,” Zaremba said, “and it’s confusing.”